Indian Digital Lending Ecosystem The digital lending industry has emerged as a crucial driver of economic growth in India, experiencing rapid advancement in recent years. The government’s strong push for...

Know moreIndian Digital Lending Ecosystem

The digital lending industry has emerged as a crucial driver of economic growth in India, experiencing rapid advancement in recent years. The government’s strong push for digitization and the development of digital infrastructure, including initiatives like IndiaStack, GST, and the Account Aggregator framework, have significantly bolstered this sector. Both banks and Non-Banking Financial Companies (NBFCs) are increasingly focusing on digital lending, collaborating with fintech companies to leverage technology and expand their reach.

Despite digital lending currently constituting a small percentage of 15% of the overall Indian lending market, its growth trajectory is promising. Ecosystem participants are capitalizing on this momentum to embark on comprehensive digital transformations, introducing innovative solutions and diversifying their offerings to capture substantial market share. The technology providers are enhancing customer experiences, digitizing the entire value chain, driving product innovation, and enabling new market segments to access lending services.

Investors

Investors have played a pivotal role in the Indian digital lending ecosystem, significantly contributing to its rapid growth and transformation. Venture capital (VC), private equity (PE), and non-banking financial companies (NBFCs) have been instrumental in fostering innovation and supporting new startups with the necessary funds for technological advancements. Despite a global slowdown in funding, India has shown resilience, with venture capital investment. This funding has been crucial for enabling fintech companies to scale and grow, even as segments have seen financing reduced in line with the overall market contraction

Going forward, investors are expected to be more discerning, focusing on fintech companies’ abilities to achieve profitability and manage non-performing assets (NPAs). Regulatory compliance has also become a critical factor, as companies that adhere strictly to regulatory norms are better positioned to navigate the financial sector’s complexities and seize long-term growth opportunities. Integrating technologies such as cloud computing, APIs, and artificial intelligence (AI) has been central to digital transformations, enhancing customer experiences, digitizing value chains, and driving product innovation. These advancements not only facilitate the entry of new market segments into the lending space but also ensure sustainable and ethical investment strategies.

Data Providers

In the dynamic landscape of the Indian digital lending ecosystem, data providers play an instrumental role in ensuring the efficiency and security of lending operations. These providers offer a wide array of services, encompassing KYC (Know Your Customer), risk management, AML (Anti-Money Laundering), and Fraud risk management (FRM), as well as Account Aggregators and Credit Information Companies. Their offerings are vital for streamlining processes, enhancing customer onboarding, and ensuring regulatory compliance. Here’s an overview of the key segments and their importance

KYC and Risk Management:

Impact: KYC and risk management are fundamental to verifying customer identities, assessing creditworthiness, and mitigating risks associated with fraud and default. Data providers in this segment streamline the onboarding process by enabling quick and accurate customer verification, thereby reducing the time and cost traditionally associated with these procedures. This results in a smoother customer experience and ensures that financial institutions comply with regulatory requirements, thereby reducing incidences of fraud and enhancing overall security.

Technological Impact: Data providers help financial institutions efficiently identify and authenticate customers by automating KYC processes and integrating various verification tools. This automation reduces manual errors and accelerates the verification process, allowing lenders to onboard customers swiftly and securely.

AML/FRM

Impact: Anti-Money Laundering (AML) and Financial Risk Management (FRM) services are critical in preventing financial crimes and maintaining the integrity of financial operations. These services include monitoring transactions in real time, conducting comprehensive risk assessments, and generating regulatory reports. By integrating these solutions, digital lenders can ensure adherence to regulatory standards, avoid penalties, and protect their reputations.

Technological Impact: AML and FRM systems continuously monitor financial transactions, identifying and flagging suspicious activities. This proactive approach allows institutions to address potential issues before they escalate, ensuring a secure and compliant lending environment.

Account Aggregator

Impact: AA enables secure financial data sharing between institutions with customer consent. This facilitates a comprehensive view of a customer’s economic situation, improving the efficiency of financial planning and lending processes. By promoting transparency and enabling open banking, these services significantly enhance financial inclusion and accessibility.

Technological Impact: Account aggregators connect multiple financial institutions, allowing for seamless data exchange. This interconnectedness gives lenders a holistic view of a borrower’s financial health, aiding in better decision-making and personalized financial advice.

Credit Bureau

Impact: Credit bureaus compile and analyze credit information from various sources to generate credit reports and scores, which are essential for evaluating the creditworthiness of borrowers. These insights help lenders make informed decisions, reduce the default risk, and offer creditworthy borrowers better terms. This promotes responsible lending practices and enhances financial stability.

Technological Impact: Credit bureaus utilize comprehensive data analytics to process credit information accurately and efficiently. This ensures that credit reports are up-to-date and reliable, providing lenders with the information to assess risk accurately.

Overall Impact

These data providers’ combined impact is transformative for India’s digital lending ecosystem. They enhance operational efficiency, reduce fraud risks, ensure regulatory compliance, and improve customer experience. By enabling faster and more accurate credit assessments, these providers help expand access to credit, particularly for underserved segments such as SMEs and individuals in rural areas. This drives financial inclusion and supports economic growth.

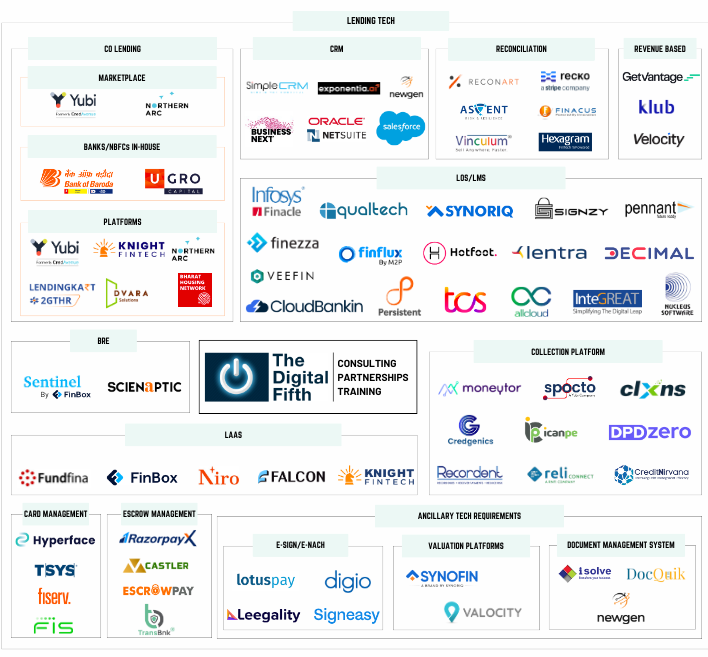

LendingTech Market Dynamics & Opportunities –

- Banks and NBFCs are gaining traction on digital lending and investing heavily in technology stacks as they see increased profitability.

- FinTech’s are accelerating their disbursements and swiftly moving towards profitability. Partnerships with FinTech’s for loan processing are improving operational efficiency for institutional lenders, resulting in reduced turnaround times and errors.

- Growing credit demand for MSMEs & continued liquidity tightening norms prompt NBFCs to go towards Co Lending model structure.

- LMS platforms will advance for multi-repayment and customizable schedules, integrating deeply with payment systems and external data sources for improved loan tracking and risk management.

- LOS designed to streamline secured lending, including property and housing loans, with improved collateral management and will innovate by integrating with Account Aggregator (AA) framework.

- With OCEN & embedded finance growth, LaaS platforms will grow.

Ancillary Tech providers –

Ancillary tech providers form the backbone of India’s digital lending framework, enabling essential services that strengthen and secure the sector. They handle key operations like appraisals, digital transactions, legal guidance, and documentation, streamlining the lending process. Their role is critical in creating a dependable digital environment where data management and transactional integrity are paramount.

In a rapidly changing financial landscape, these providers are essential for innovation, quickly adapting to new challenges and needs. They enhance customer interaction, improve risk assessment, and boost the efficiency of financial operations. Through their support, they drive the financial sector’s growth, encouraging broader access to finance and laying the groundwork for future digital advancements.

Financial Inclusion

The future of financial inclusion in India is poised for transformation, driven by digital innovations and a strategic focus on underbanked and unbanked sectors, including rural, tier 2-3 cities, and groups such as Self-Help Groups (SHGs) and Joint Liability Groups (JLGs). The utilization of alternate data will be crucial in this segment, with investors keeping a close eye and players needing to navigate regulatory requirements for long-term sustainability.

It’s crucial to augment these platforms’ security to foster user trust and encourage their widespread use. Continuous investments by the government in artificial intelligence (AI) are anticipated to drive innovation and bolster security against increasingly complex fraudulent schemes, including the potential establishment of a dedicated cyber-fraud agency to protect consumers and mitigate online fraud risks.

Furthermore, the expansion of retail agent networks is essential for extending financial services to remote locations, lacking in traditional banking facilities. These agents are vital in connecting financial institutions with individuals, thereby making financial services accessible to a wider audience.

The focus should be on improving credit availability to underserved populations in tier-2 and tier-3 areas and the over 64 million MSMEs. Implementing measures like a unified ‘One KYC’ repository could drastically streamline the onboarding process and reduce process redundancies, making it easier for individuals to access the financial system. Improving data access for credit assessments is crucial for enabling financial institutions to offer loans more effectively, which in turn would support economic development and empower more individuals financially

Financial Institutions –

Banks and Non-Banking Financial Companies (NBFCs) form the backbone of the lending sector because of regulatory license holders for lending. These regulated entities operate under close monitoring and strict compliance with RBI regulations and contribute a significant portion of the lending capital and cater to credit risk in the market. Banks and NBFCs also play major roles in supporting Fintech-driven business models by being their lending partners.

Being there in existence for a long, the players in the Banking layer hold a large consumer base yet they aren’t accessible to everyone. Still, large segments of the population, especially Thin files customers, MSME segments remain deprived of credit. This gap has largely been attempted by the Fintech players which enable their access to untapped segments of the market.

Although customers continue to place significant trust in traditional banks, Fintech companies have been able to attract customers for their loan requirements due to their technological advancements, such as use of data analytics, etc. FinTech’s have been able to enhance customer service by providing a comprehensive, holistic understanding of the customer and enabling faster and more efficient assistance. FinTech’s have largely been partnering with Banks to support digital lending growth in the country.

Embedded Finance

Embedded finance is revolutionizing the financial sector by integrating financial services into non-financial platforms, facilitated through partnerships between financial institutions (FIs) and fintech organizations. This collaboration leverages Banking as a Service (BaaS), Lending as a service (LaaS), Payment as a service (PaaS) etc solutions, enabling the seamless creation of financial products that can be directly incorporated into various apps and services, aiming to significantly impact the Indian financial market by 2024.

Key Market Dynamics –

- The growth of this trend is largely driven by the availability of API-based modular products, which provide easy access to financial services across different sectors, notably e-commerce, offering benefits like instant loans and digital FDs without a bank account.

- E-commerce players lead the embedded finance market with their Pay Later and Credit Card products driven by deep integrations with lenders.

- LaaS providers enable Fintech and Embedded Finance players to provide credit by offering plug-and-play tech stacks.

- Decoupling of the Engagement layer (i.e. shifting to Embedded Finance players) & banking layer is creating an opportunity for Anything as A Service i.e. XaaS.

- Banking (BaaS), Lending (LaaS) and Payments (PaaS), have emerged as key areas of investment for VCs.

BNPL

A noteworthy trend in the Indian lending space is the massive demand for credit in tier-2, tier-3 cities, and beyond, where consumers, often ‘new to credit’ or with limited credit histories, are increasingly turning to BNPL services for small-ticket credit needs. This demand underlines the need for customized BNPL products catering to varied consumer requirements across different segments. BNPL will continue to grow, banks of all sizes will partner with fintech’s resulting in mutually beneficial partnerships for example SBM bank partnered with Lazy pay as well as new innovations are also anticipated in this segment

India’s regulatory environment, led by the Reserve Bank of India (RBI), has played a pivotal role in shaping the BNPL and broader digital lending sector by providing a stable regulatory framework conducive to growth and innovation.

Supply Chain Finance

Supply Chain Finance (SCF) in India is rapidly evolving as a key innovation to boost liquidity and strengthen supply chains, offering significant benefits to small and medium-sized enterprises (SMEs) that face hurdles in accessing traditional credit. By facilitating early invoice payments at a discount for suppliers and allowing buyers to extend payment terms, SCF effectively optimizes working capital. This foundational strategy is now expanding into Deep Tier Financing (DTF), which broadens the scope of SCF to include not only immediate suppliers and buyers but also the extensive network of upstream suppliers (tier 2 and beyond). Aimed at addressing the comprehensive liquidity needs within the supply chain, DTF is especially crucial for supporting SMEs located deeper within the supply chain, who often face more substantial financing challenges. This evolving approach is gaining momentum, propelled by collective efforts from businesses and financial institutions to enhance supply chain resilience and sustainability.

Looking ahead, the future of Deep Tier Supply Chain Finance appears promising. The notable contribution of MSMEs to both national and global GDP underscores the necessity for a robust and efficient supply chain across various sectors, including exports and manufacturing. As the scenario unfolds, increased competition is expected to accelerate the pace of innovation, leading to more customizable options and innovative financing solutions for stakeholders across all tiers, further enabling a thriving ecosystem for supply chain finance in India.

TREDS

The segment also includes Trade Receivables and Discounting System (TReDS) companies which is an electronic platform for facilitating the financing/discounting of trade receivables of MSMEs through multiple financiers. These receivables can be due from corporates and other buyers, including Government Departments and Public Sector Undertakings (PSUs).

Loan Market Place

With the lending ecosystem adding new players every day, borrowers are often confused about which lender to avail credit from. This is where a loan marketplace comes in. These platforms allow borrowers to compare the loan products offered by different vendors and choose the one that best suits their needs. These marketplaces also play a role in ensuring that the borrower receives a competitive interest rate for his loans.

RELATED POSTS

Insurtech Eco-System: Transforming India’s Insurance Landscape

Insurtech Eco-System: Transforming India’s Insurance Landscape The insurtech industry in India is experiencing a significant transformation, driven by technological advancements and increased digital adoption. The government’s push for digitization and initiatives such...

Know more

Open Network for Digital Commerce

Open Network For Digital Commerce The Open Network for Digital Commerce (ONDC) is transforming India’s e-commerce landscape by democratizing market access and fostering financial inclusion. Connecting 30 million sellers with...

Know more