Indian Digital Lending Ecosystem The digital lending industry has emerged as a crucial driver of economic growth in India, experiencing rapid advancement in recent years. The government’s strong push for...

Know moreOverview of Credit Cards and Business Model

Credit cards have become an integral part of the modern financial landscape, offering convenience and flexibility to consumers while also driving significant revenue streams for financial institutions. In India, credit cards are issued primarily by banks and select NBFCs to eligible individuals, allowing them to make purchases on credit with the promise of repayment at a later date. This is not just a tool for transaction convenience but a robust system that includes rewards programs, credit-building opportunities, and fraud protection measures. The total credit cards in circulation currently amount to 10 Crore.

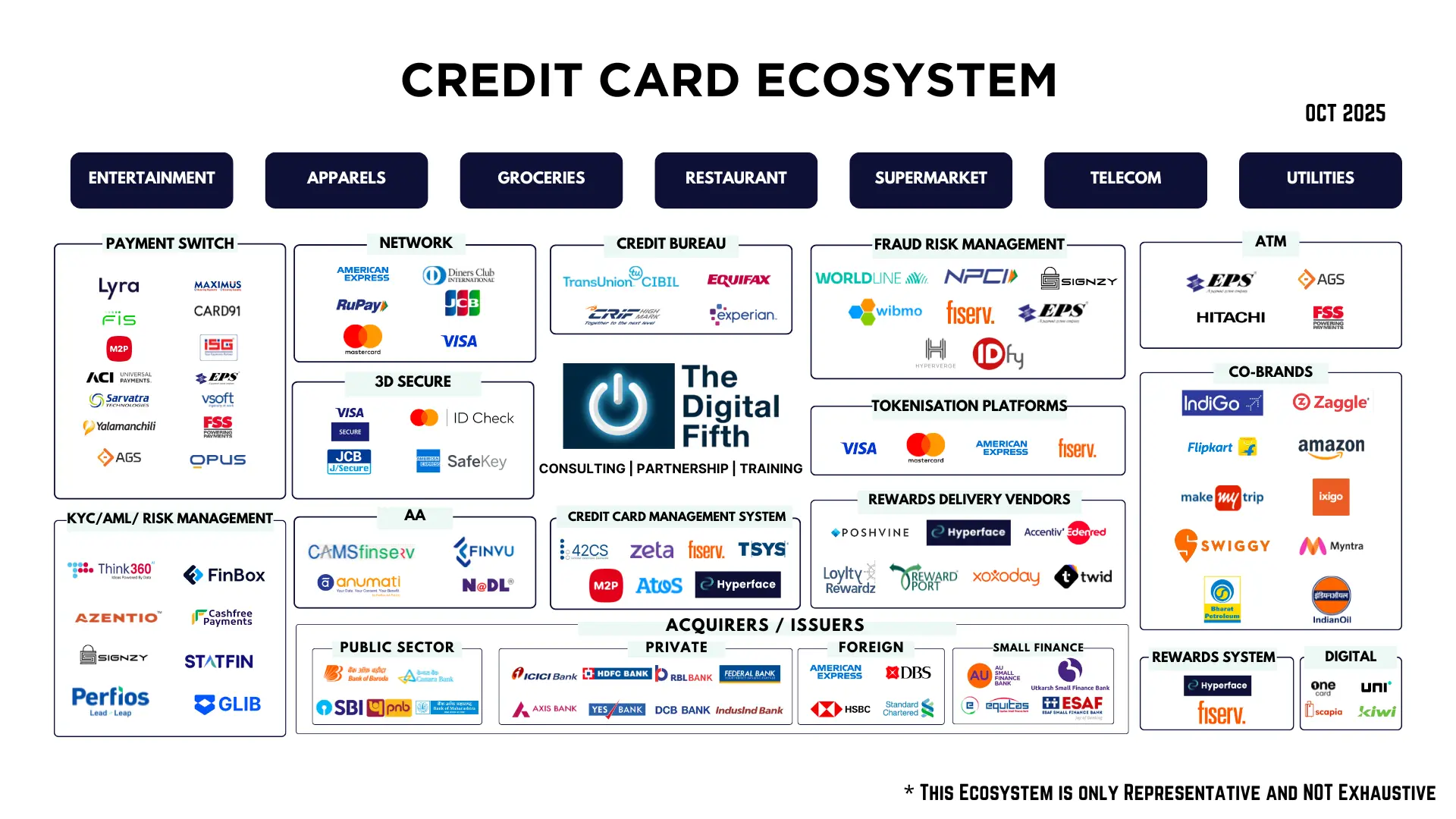

The credit card ecosystem in India encompasses a broad range of stakeholders including banks, non-banking financial companies (NBFCs), payment networks like Visa and MasterCard, merchant acquirers, and fintech companies. These players collaborate to provide seamless transaction experiences while ensuring security and compliance with regulatory standards.The ecosystem of credit cards in India is multifaceted, involving various stakeholders and processes. Key components of the credit card ecosystem include:

Key Components of the Credit Card Ecosystem

The credit card ecosystem revolves around several key components:

- Issuing Banks: Banks issue credit cards to customers after assessing their creditworthiness and ability to repay debt. These banks earn revenue through interest charges, annual fees, late payment fees, and other charges associated with credit card usage.

- Acquiring Banks: Acquiring banks partner with merchants to process credit and debit card payments. They provide the technology and financial infrastructure necessary for conducting transactions and collecting fees for each transaction processed, sharing a portion of these fees with the card networks and issuers.

- Merchant Network: Credit card companies establish partnerships with merchants to accept card payments. Merchants benefit from increased sales and customer convenience, while credit card companies earn transaction fees on every purchase made using their cards.

- Card Networks: Visa, Mastercard, American Express, and RuPay are some of the major card networks operating in India. These networks facilitate transactions between issuing banks, acquiring banks (merchants’ banks), and cardholders, earning interchange fees in the process.

- Rewards and Incentives: To attract customers and encourage card usage, banks offer rewards, cashback, discounts, and other incentives to cardholders for spending on their credit cards. These rewards are funded through interchange fees and interest charges.

- Regulatory Authorities: Regulatory bodies like the Reserve Bank of India (RBI) play a crucial role in overseeing the credit card industry, setting guidelines, and enforcing regulations to ensure consumer protection, fair practices, and financial stability.

Key Components of Credit Card Business Model

The Technology Partners and Revenue Streams:

- Credit Card Management System: Credit card management systems handle administrative tasks such as account management and transaction processing. They generate revenue either through subscription fees charged to banks and financial institutions, transaction fees per transaction processed, and sales of software licenses along with maintenance and support services.

- Payment Switch: Payment switches facilitate the routing of transaction data between banks and payment networks, earning revenue primarily through per-transaction fees. They also generate income from integration services and ongoing system maintenance fees provided to banks and merchants.

- Network: Card networks like Visa, Rupay, and Mastercard provide infrastructure for processing transactions and earn revenue from interchange fees charged on each transaction, assessment fees based on transaction volume, and licensing fees for using their network and brand.

- Credit Bureau: Credit bureaus collect individual credit histories and generate revenue by selling credit reports and scores to financial institutions and sometimes consumers. They also offer analytical services for risk assessment, contributing further to their revenue streams.

- Rewards System: Rewards systems manage and track credit card rewards programs, earning revenue through service fees charged to banks for managing these programs. They also make money from partnerships with merchants who participate in offering rewards and promotions.

- Rewards Delivery Vendors: Rewards delivery vendors fulfill the delivery of rewards like goods, services, or digital items. They generate revenue by charging service fees to financial institutions for the distribution and handling of these rewards, ensuring efficient and accurate reward fulfillment.

Growth Factors

The sector has experienced substantial growth, with a significant uptake in adoption post-digitalization and through government initiatives such as the zero MDR policy. Innovations in technology, such as the adoption of contactless payments, Advanced Encryption Standards, Behavioral Biometrics, and security enhancements like Two-Factor Authentication, have further bolstered consumer trust and usage. The explosive growth of e-commerce, especially in the wake of increased internet penetration and smartphone usage, has significantly contributed to the rise in credit card usage. Cards tailored with travel benefits and comprehensive rewards programs have become highly attractive, especially to the middle and upper classes who travel frequently and spend on leisure.

- Shift Toward Cashless Transactions: There’s a growing preference for cashless transactions among consumers for reasons of convenience, safety, and new buying behaviors, which encourages credit card use.

- Zero MDR Policy: The implementation of a zero Merchant Discount Rate (MDR) policy for RuPay card transactions helped to promote digital transactions through cards.

- Fintech Partnerships: Collaborations between traditional banks and fintech firms have introduced innovative products that cater to a tech-savvy generation.

- Preference for Credit over Debit: Consumers increasingly prefer credit cards over debit cards due to the additional benefits such as credit building, deferred payments, and rewards.

- Increased Online Retail: With more consumers shopping online, credit cards become a preferred method of payment due to their ease of use and consumer protection features.

Key Players

- Major Banks: HDFC, ICICI, SBI, and Axis Bank leading the market, constantly innovating in terms of product offerings and customer service.

- Payment Networks: Facilitate transactions and ensure interoperability among different financial institutions.

- Fintech Innovations: Such as OneCard offers a card integrated with an app that provides full control over the card features, including real-time spend tracking, and flexible reward point redemption.

Regulatory Framework Around Credit Cards and Its Implications

The regulatory framework Master Direction – Credit Card and Debit Card – Issuance and Conduct Directions, 2022 (Updated as of March 07, 2024) governing credit cards in India aims to safeguard the interests of consumers, promote transparency, and maintain the stability of the financial system. The Reserve Bank of India (RBI), as the country’s central bank, plays a pivotal role in formulating and enforcing regulations related to credit cards. The regulatory framework addresses various facets of credit card operations, including the issuance, management, and grievance redressal processes. Some key aspects of the regulatory framework include:

- Guidelines: The RBI sets guidelines for banks and financial institutions issuing credit cards. These norms cover aspects such as credit risk management, capital adequacy, provisioning requirements, and exposure limits to mitigate the risk associated with credit card operations.

- Fair Practices Code: The RBI mandates banks to adhere to a Fair Practices Code while issuing credit cards to customers. This outlines principles of transparency, confidentiality, grievance redressal, and responsible lending to ensure fair treatment of cardholders.

- Interest Rate Regulation: The RBI regulates the interest rates charged on credit card outstanding balances to protect consumers from exorbitant charges and predatory lending practices. Banks are required to disclose the annual percentage rate (APR) and other fees associated with credit cards transparently.

- Security Standards: To enhance the security of credit card transactions, the RBI mandates the implementation of robust security measures such as two-factor authentication (2FA), encryption, and tokenization. These measures help prevent fraud, unauthorized transactions, and data breaches.

- Customer Protection: The regulatory framework emphasizes consumer protection measures, including dispute resolution mechanisms, liability limits for unauthorized transactions, and the provision of clear and concise terms and conditions to cardholders. Banks are required to promptly address customer complaints and grievances.

Implications of the Regulatory Framework

The regulatory framework surrounding credit cards in India has several implications for both consumers and financial institutions:

- Consumer Protection: Regulations aimed at enhancing consumer protection ensure that cardholders are treated fairly, provided with transparent information, and protected against abusive practices. This instills confidence in the credit card system and promotes responsible credit usage.

- Risk Management: The guidelines prescribed by the RBI help banks manage credit risk effectively, maintain adequate capital buffers, and prevent excessive exposure to risky assets. By adhering to these, banks can mitigate the risk of credit card defaults and delinquencies.

- Compliance Costs: Financial institutions incur costs related to compliance with regulatory requirements, including implementing security measures, conducting audits, and training staff. While compliance costs may increase operational expenses, they are essential for maintaining regulatory compliance and ensuring the integrity of the credit card ecosystem.

- Innovation and Competition: Regulatory frameworks that strike a balance between consumer protection and market efficiency foster innovation and competition in the credit card industry. Banks and fintech companies are encouraged to develop innovative products, services, and technologies that cater to evolving consumer needs while complying with regulatory standards.

- Market Conduct and Ethics: Adherence to fair practices codes and ethical conduct guidelines promotes trust and integrity in the credit card market. Financial institutions that uphold high standards of market conduct are better positioned to attract customers, build long-term relationships, and sustainably grow their business.

Emerging Trends in the Credit Card Industry

The credit card industry in India is witnessing several emerging trends driven by technological advancements, changing consumer preferences, and regulatory developments. Some notable trends include:

- Contactless Payments: The adoption of contactless payment technology, enabled by Near Field Communication (NFC) and mobile wallets, is rapidly gaining traction among Indian consumers. Contactless cards and mobile payment apps offer convenience, speed, and enhanced security, driving the shift towards cashless transactions.

- Digital Banking Platforms: Banks and fintech companies are leveraging digital banking platforms to offer seamless and personalized credit card experiences to customers. Digital onboarding, real-time account management, and AI-powered insights enhance user engagement and satisfaction.

- Tokenization: In the financial sector banks aim to utilize tokens to replace sensitive card details with a non-sensitive equivalent, known as a token. These tokens can safely be passed through the internet without actual bank details being exposed

_(1).png)

- Data Analytics and AI: Data analytics and artificial intelligence are being used to analyze customer spending patterns, detect fraud, and personalize credit card offerings. Predictive analytics and machine learning algorithms enable banks to tailor rewards, promotions, and credit limits based on individual preferences and behavior.

- Regulatory Innovation: Regulatory authorities are embracing technology and innovation to enhance regulatory oversight, streamline compliance processes, and promote financial inclusion. Initiatives such as regulatory sandboxes, open banking frameworks, and digital identity verification facilitate responsible innovation while safeguarding consumer interests.

- Sustainability and ESG: There is growing emphasis on environmental, social, and governance (ESG) factors in the credit card industry. Banks are launching eco-friendly credit cards, virtual credit cards offering rewards for sustainable spending, and implementing ESG criteria in credit underwriting and risk assessment.

Conclusion

The credit card industry in India is set for a transformative journey with continued growth driven by innovation, regulatory support, and technological integration. The interplay between regulatory policies and market trends will be crucial in shaping an ecosystem that is both vibrant and secure, offering enhanced value to consumers and contributing positively to the broader financial landscape in India. The continuous evolution in regulatory practices and consumer technology adoption will dictate the strategic directions of credit card issuers and their approaches to meeting the changing needs of Indian consumers.

As we continue to navigate the dynamic landscape of the credit card industry in India, our company remains at the forefront, providing comprehensive services tailored to help you stay ahead. With expertise in benchmarking, regulatory compliance, product development, and program management, we are equipped to enhance your offerings and ensure they meet the highest standards of innovation and regulation. Partner with us to leverage our industry insights and expertise, and together we can shape a future that exceeds your expectations. Let’s connect to discuss how we can support your business in these exciting times.

Watch our webinar

RELATED POSTS

Insurtech Eco-System: Transforming India’s Insurance Landscape

Insurtech Eco-System: Transforming India’s Insurance Landscape The insurtech industry in India is experiencing a significant transformation, driven by technological advancements and increased digital adoption. The government’s push for digitization and initiatives such...

Know more

Open Network for Digital Commerce

Open Network For Digital Commerce The Open Network for Digital Commerce (ONDC) is transforming India’s e-commerce landscape by democratizing market access and fostering financial inclusion. Connecting 30 million sellers with...

Know more