Most compliance failures aren’t policy issues - they’re execution gaps. Learn why compliance breaks on the ground and how to...

Know moreThe Evolution of Credit Cards: Future of Digital Payments in India and Innovations in Reward Programs

Credit Cards and its adoption in India

Credit cards have continued to revolutionize the way we manage money and make purchases, becoming an essential part of daily transactions in India’s rapidly evolving cashless economy. Offering both convenience and security, they have gained widespread acceptance across diverse consumer segments.

But what makes credit cards so appealing? Beyond their ease of use, they come packed with rewards programs and exclusive benefits that add to the purchase experience. As digital payments continue to transform the financial landscape, this paper looks into understanding emerging trends within Credit Cards and of the evolution of credit card rewards

Emerging Landscape of Credit Card Ecosystem

India’s credit card ecosystem comprises of a dynamic network of banks, NBFCs, payment networks like Visa, Rupay and MasterCard, merchant acquirers, and fintech innovators. These stakeholders collaborate to drive seamless transactions, enhance security, and ensure compliance with evolving regulations. As digital payments accelerate, the ecosystem continues to expand, shaping the future of financial services.

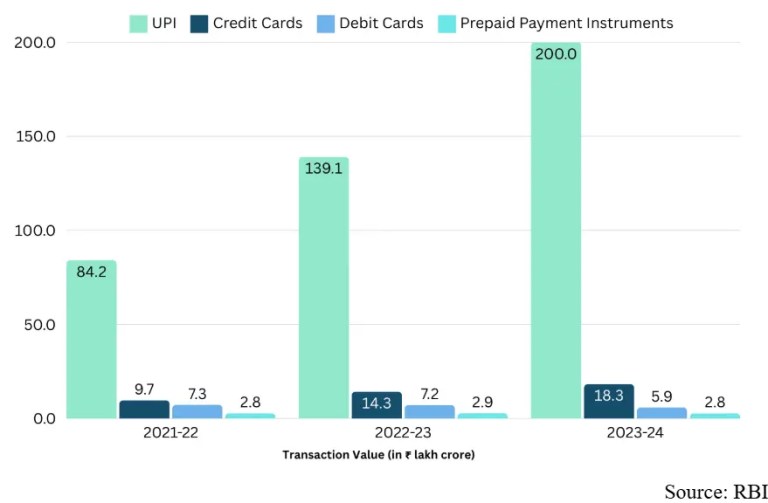

Impact of Digital Payments in India

The rapid growth of digital payments in India has reshaped the credit card industry, with UPI and mobile wallets becoming the go-to payment methods for millions. As more consumers prefer seamless, cashless transactions, traditional credit cards are facing new competition.

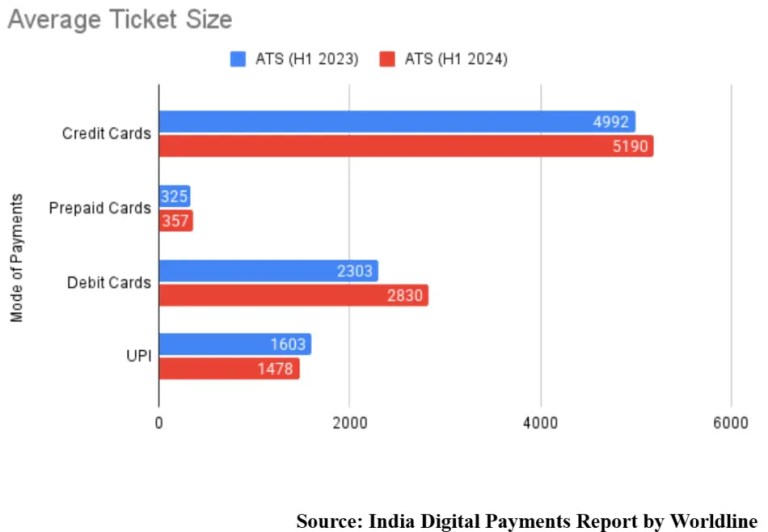

While we see transaction volumes increasing, here is the Average Ticket Size (ATS) across different payment modes, showcasing year-over-year changes in spending behavior.

Regulatory Guidelines and Their Impact

The Reserve Bank of India (RBI) has introduced new guidelines to enhance transparency, security, and customer protection in the credit card industry. Key regulatory updates include:

Guidelines on Credit Cards: RBI’s recent regulations mandate clear disclosures on fees, interest rates, and billing cycles, ensuring better customer awareness and preventing hidden charges. Additionally, card issuers must obtain explicit consent before increasing credit limits or charging fees.

Co-Branded Credit Card Regulations: RBI has set stricter norms for co-branded credit cards, requiring banks to have greater control over customer relationships and ensure compliance with data protection laws reinforcing the bank’s accountability.

These regulatory measures aim to make credit cards more customer-friendly and secure, helping the industry adapt to the evolving digital payment ecosystem while maintaining trust and compliance.

Strategies Adopted by Credit Card Companies to Stay Relevant

With the rapid rise of digital payments, credit card companies are continuously innovating to retain their relevance in an increasingly UPI-dominated ecosystem. Rather than being replaced, credit cards are evolving to offer enhanced convenience, security, and affordability.

Key strategies include:

UPI Integration: The RuPay network now allows users to link credit cards to UPI, making payments even more convenient and expanding the usability of credit cards in digital transactions.

Better Rewards & Benefits: Many credit card companies are offering higher cashback and reward programs for digital transactions to encourage card usage.

Popularity of EMI on Credit Cards: With rising consumer demand for affordability, credit card issuers have made EMI (Equated Monthly Installment) options more accessible. Many banks offer instant EMI conversion on large transactions, making high-value purchases more manageable. No-cost EMI and flexible repayment tenures have further boosted credit card usage.

Tokenization: To enhance security and convenience, credit card companies have embraced tokenization, where actual card details are replaced with a unique token for transactions. For ex. Google Pay now supports the addition of credit cards, allowing users to make secure tap-and-pay transactions using their smartphones while keeping their card details protected.

By leveraging these strategies, credit card providers are ensuring that they remain a preferred payment option in India’s evolving digital finance landscape

The Impact of Credit Cards on UPI and What It Means for Users

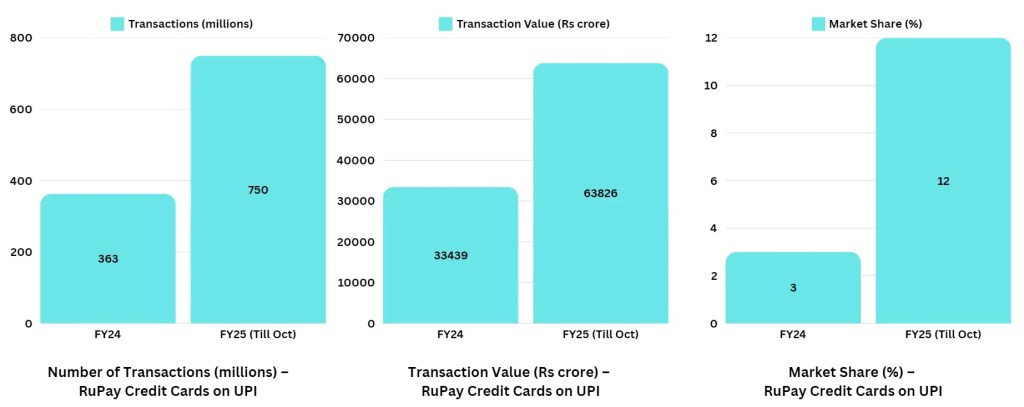

A major development in this space is the integration of credit cards with UPI. In 2022, the Reserve Bank of India (RBI) allowed the linking of RuPay credit cards to UPI, enabling users to make UPI transactions while drawing from their credit limit.

Credit Card to UPI: A Simple Guide

Linking your credit card to UPI is easier than ever, thanks to tokenization—a process that replaces your actual card details with a secure digital token. Currently, this feature is primarily available for RuPay credit cards, launched by the National Payments Corporation of India (NPCI) in collaboration with banks. Once linked, you can seamlessly use your credit card for UPI payments.

Benefits of Linking Your Credit Card to UPI

Linking credit cards to UPI is a major step forward in India’s digital payments space, bringing together the convenience of UPI with the flexibility of credit. This innovative feature offers several advantages:

Benefits for Consumers

More Payment Flexibility: No need to rely solely on bank balances; use your credit card for everyday UPI transactions.

Earn More Rewards: Credit card payments on UPI mean more cashback, discounts, and loyalty points from banks and merchants.

Convenience: Make quick, contactless payments at both online and offline stores.

Benefits for Merchants

Boost in Sales: Accepting credit cards via UPI attracts more customers, increasing transaction volume.

Lower Transaction Costs: Compared to traditional credit card machines, UPI-based payments may reduce fees for businesses.

Faster Settlements: UPI payments settle quickly, improving cash flow for merchants.

The Evolution of Credit Card Reward Programs

Credit card reward programs have come a long way since their introduction. Initially, they primarily offered cashback or discounts on purchases. These basic incentives quickly gained popularity among consumers seeking value in every transaction.

As competition intensified, credit card issuers began to innovate. Points systems emerged, allowing users to accumulate points for travel, shopping, and dining experiences. This shift transformed the landscape of loyalty schemes.

Today, we see tailored rewards that cater to individual spending habits. For instance, some cards offer elevated rewards for groceries or fuel purchases, while others focus on travel perks or exclusive access to events.

The rise of co-branded credit cards further illustrates this evolution. Partnerships with airlines, hotels, e-commerce merchants and retail brands provide additional benefits like free flights, accommodation upgrades, and exclusive discounts—an option for frequent travelers and brand-loyal consumers.

As consumer expectations evolve alongside technology advancements, the future of these programs promises even more personalization and dynamism.

Types of Credit Card Rewards: Find the Best Perks for Your Spending

Credit card rewards come in various forms, catering to different spending habits and lifestyles. Whether you prefer cashback, travel perks, or category-specific rewards, there’s a card for you.

1. Cashback Rewards

One of the most popular reward types, cashback credit cards offer a percentage of your spending back as cash. This is perfect for everyday expenses, as the cashback earned is often directly deducted from your next billing cycle, effectively lowering your monthly bill.

2. Travel Rewards

Frequent travelers benefit from travel rewards credit cards, which offer points or miles redeemable for flights, hotel stays, and car rentals. Many banks also provide point transfer options for accelerated redemptions through partner websites.

3. Category-Based Rewards

Some credit cards specialize in dining, groceries, or fuel, offering higher reward rates in these categories. For example, certain grocery and food delivery credit cards provide instant discounts and cashback, applied directly to your next bill.

4. Hybrid Reward Cards

For those who prefer flexibility, hybrid rewards cards combine multiple benefits, letting users earn both cashback and points across various spending categories.

5. UPI Rewards

With the rise of credit card payments on UPI, banks are now offering 0.5%–1% cashback on UPI transactions powered through Credit cards, making digital payments even more rewarding.

Co-Branded Credit Cards: Exclusive Perks with Partner Brands

Co-branded credit cards have gained immense popularity in India, offering users specialized benefits tied to specific brands. These cards are issued in partnership with airlines, retail chains, ,e-commerce , marketplaces ,fuel companies, and digital platforms to enhance customer loyalty and spending incentives.

Market Insights & Growth Trends

Expanding Market Size: The co-branded credit card segment is growing rapidly esp post detailed guidelines released by regulator, driven by increased consumer spending and brand collaborations. In India, co-branded credit cards contribute to a significant portion of new credit card issuances, particularly in travel, retail, and e-commerce segments.

High Customer Engagement: Studies indicate that users of co-branded credit cards tend to have higher spending patterns, with loyalty-driven customers using these cards for 50-60% of their total monthly expenses in the respective category (e.g., airline, retail, or fuel).

E-Commerce & Digital Platforms Leading Growth: With the boom in online shopping, fintech partnerships with banks have surged. Leading e-commerce giants like Amazon, Flipkart, have launched highly rewarding co-branded credit cards in partnership with ICICI Bank, Axis bank respectively, offering instant discounts and cashback.

Increased Partnerships in Travel & Hospitality: With the revival of the travel industry post-pandemic, banks are partnering with airlines and hotel chains to offer cards with free flight tickets, lounge access, and priority bookings. For example, leading Indian airlines have introduced co-branded cards with benefits like complimentary tickets and tier upgrades.

The Future of Digital Payments and Credit Card Rewards

The future of digital payments is set for rapid transformation, driven by technological advancements and evolving consumer preferences. While UPI continues to dominate small-ticket transactions in the person-to-merchant (P2M) space, credit cards will remain the preferred choice for high-value purchases, such as e-commerce, travel, and electronics.

Personalized Rewards and AI-Driven Insights

The future of credit card rewards lies in seamless personalization, driven by advanced data analytics and AI. Banks will leverage these technologies to offer tailored cashback, exclusive discounts, and customized loyalty benefits, making reward programs more relevant and valuable to consumers.

The Role of AI in Fraud Detection and Customer Experience

As digital transactions grow, security remains a top priority. AI-powered fraud detection systems will analyze user behavior in real time, reducing the risk of fraudulent activities. Additionally, AI will enhance customer experiences by recommending smarter rewards and optimizing credit utilization based on spending habits.

Contactless Payments and Integrated Loyalty Programs

With increasing adoption of contactless payments via smartphones and smartwatches, credit card issuers have an opportunity to design innovative loyalty programs linked directly to daily spending patterns. This could mean instant rewards on grocery purchases, exclusive deals on travel bookings, or higher cashback on digital transactions.

Conclusion

As we look to the future, it’s clear that credit cards and digital payments are evolving at an unprecedented pace. The innovations in reward programs reflect a shift towards more personalized and dynamic offerings, catering to individual spending habits and preferences.

As consumers become increasingly tech-savvy, financial institutions must adapt by integrating advanced technologies like AI and machine learning into their rewards strategies to deliver tailored cashback, exclusive discounts, and loyalty benefits in real-time.

The rise of digital payments is reshaping how we think about transactions. With options like using credit cards on UPI gaining traction, convenience is becoming paramount for consumers everywhere. This trend signals a move toward seamless, reward-driven payment experiences, where speed, efficiency, and value-added benefits play a crucial role.

Looking ahead, the synergy between credit card rewards and digital payment systems will likely deepen. Expect to see greater integration with enhanced security features, and real-time tracking of reward earnings, making every transaction more rewarding. Banks and financial institutions will continue innovating, ensuring that consumers receive maximum value from their spending through personalized rewards, milestone benefits, and exclusive merchant partnerships.

RELATED POSTS

The Corporate Card Opportunity Nobody’s Talking About | The Next B2B Fintech Infrastructure Play

Corporate cards for SMEs could become the next major fintech infrastructure play. Explore how B2B cards, spend management platforms, and...

Know more

Data Readiness in BFSI: Building the Intelligence Layer for AI

India’s BFSI sector is shifting from data accumulation to intelligence-ready infrastructure. Explore how real-time pipelines, lakehouses, and governance power AI.

Know more