Table of Contents

Introduction

Over the past few years, the relationship between Indian banks and fintechs has evolved from cautious cooperation to intentional co-creation. What began with white-label cards and API collaborations is giving rise to a new era of co-brand innovation, where banks and fintechs work together to develop products, experiences, and ecosystems that redefine customer involvement.

In the banking industry, co-branding refers to a card’s logo or reward-sharing scheme. These days, it represents something far deeper: a set of abilities. Fintechs provide customer-centric design, agility, and data-driven personalization. Banks provide trust, scale, and regulatory depth. A successful combination of these produces an ecosystem as opposed to a single product.

When done correctly, co-brand innovation can open up completely new markets, increase reach, and improve financial experiences.

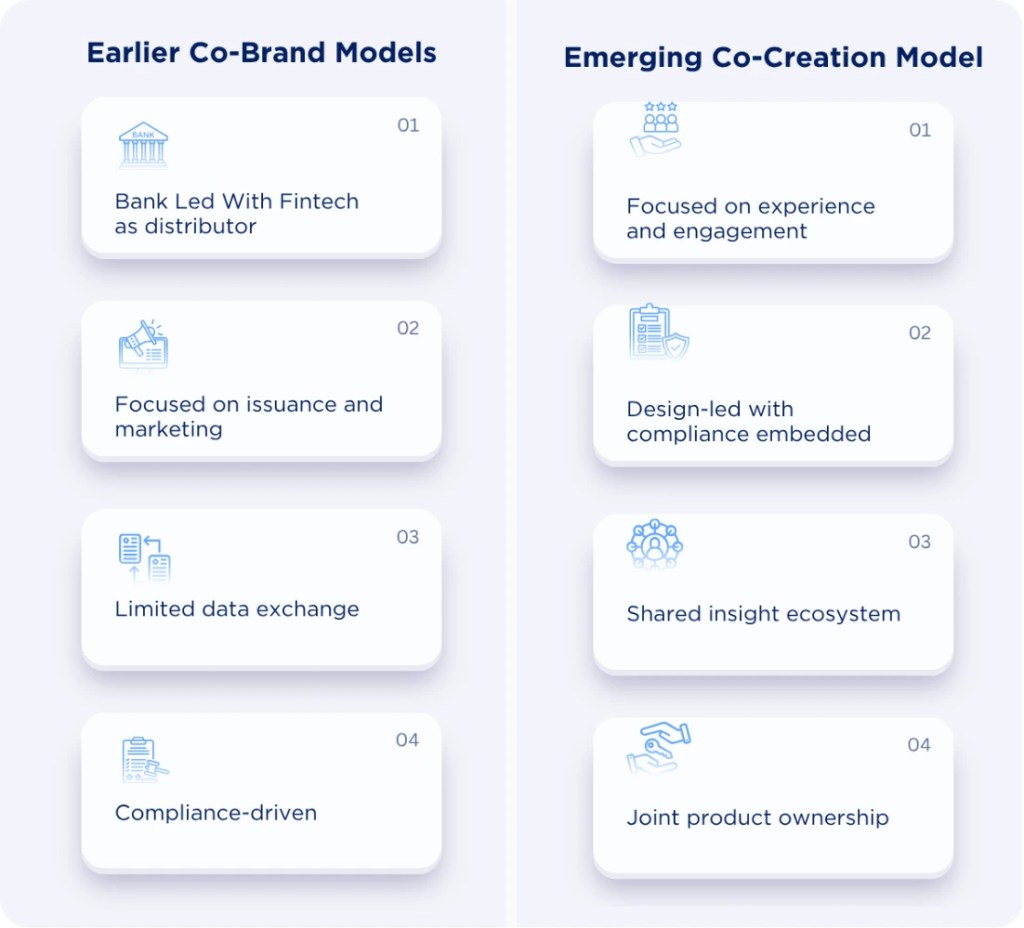

From Co-Branding to Co-Creation

Co-branded alliances in the past were mostly transactional. The bank supplied the infrastructure and licensing, while a fintech company handled customer acquisition. After the card or account went live, the partnership was terminated.

Leading companies are already embracing co-creation, working together to define digital interfaces, customer experiences, and even common data frameworks. With this progression, distribution relationships give way to experience partnerships.

As integrated finance expands into retail, travel, and e-commerce, co-branding is evolving into a strategic business tool that is altering how customers interact with financial products.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

Lessons Fintechs Can Teach Banks About Co-Brand Innovation

Several common themes have arisen from bank-fintech partnerships in India. These are about reconsidering the essence of innovation, not just technology.

- 1. Build Fast, Learn Faster

Fintechs like OneCard, Jupiter, and Fi Money built their early success by rapidly iterating on design, onboarding, and feature sets. Their approach launches fast, measure, and refine contrasts with the traditional banking mindset of waiting for perfection before release.

What banks can adopt:

- Create controlled sandboxes for co-brand pilots with pre-approved risk parameters.

- Adopt a minimum viable product (MVP) frameworks that focus on solving one problem well before expanding features.

- Embed joint experimentation cells within partnership governance structures to shorten time-to-market.

- 2. Design Around Customers, Not Compliance

Fintechs start from the customer’s life moment, paying, saving, borrowing, and build backward. Banks often start with process and policy. The most successful co-brand innovations blend both worlds.

What banks can adopt:

- Begin co-brand journeys with customer journey mapping rather than product specification.

- Integrate real-time UX testing into product design cycles.

- Build compliance frameworks into design so regulations guide the experience instead of limiting it.

Example: A leading bank redesigned account onboarding from the customer journey outward, turning a multi-day, document-heavy process into a five-minute mobile experience with built-in video ID, liveness checks, and contextual disclosures, embedding compliance into the design rather than treating it as a constraint.

- 3. Use Data as a Co-Brand Differentiator

Fintechs flourish in the era of open data by contextualizing and personalizing products with insights. The real-time intelligence layer that fintechs provide is what banks lack, despite having extensive transactional datasets already.

What banks can adopt:

- Leverage Account Aggregator (AA) frameworks to enable consent-based data sharing for co-brand personalization.

- Build joint data lakes with fintech partners under clear governance to power rewards, offers, and credit models.

- Move from static segmentation (income, geography) to behavioral segmentation (spend pattern, channel preference).

Example: The ICICI Bank–Amazon Pay Credit Card uses transaction-level insights from Amazon’s platform to segment users and push targeted offers. This cashback structure leverages behavioral spend data to differentiate the co-brand experience.

Source – ICICI Bank

- 4. Culture and Agility

The most challenging aspect of a co-brand journey culture is rarely integrating technology. Banks use layered governance structures, while fintechs use agile sprints. When these perspectives diverge, innovation stalls.

What banks can adopt:

- Build Collaborative teams that include fintech product managers and bank risk/compliance officers working together from day one.

- Define clear ownership structures, banks anchor governance, fintechs lead customer experience.

- Introduce shared KPIs tied to user activation, not just product rollout.

Example: Suryoday Small Finance Bank’s partnership with Paytm to launch a Credit Line on UPI demonstrates how a regulated bank and a fintech can jointly deliver innovation with speed and compliance. The collaboration leveraged Suryoday’s governance and Paytm’s technology capabilities to roll out a postpaid product in a fast and compliant manner.

Source – Suryoday Bank

- 5. Think Ecosystem, Not Just Product

Fintechs rarely stop at one product they build ecosystems. Successful co-brands in India are doing the same.

What banks can adopt:

- View co-brand launches as platform foundations, not one-off products.

- Enable modular APIs so partners can plug in lending, rewards, and credit seamlessly.

- Measure success by lifetime engagement, not issuance volume

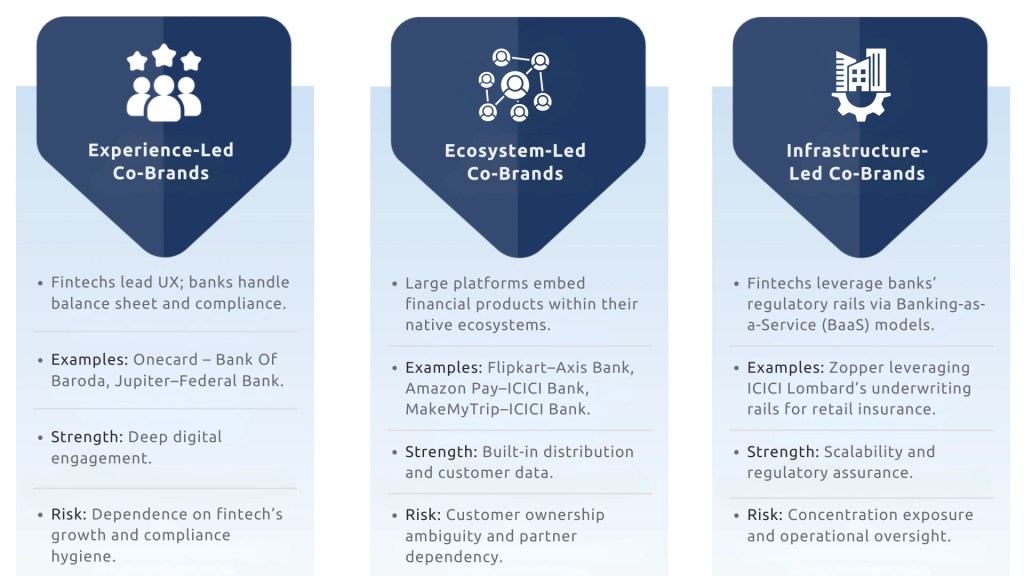

Models of Co-Brand Innovation Emerging in India

India’s financial ecosystem is witnessing the rise of three broad co-brand models each with distinct strengths and risks:

Each model shows that co-brand success is not about brand fit, it’s about operational clarity, data sharing discipline, and cultural alignment.

What Banks Bring to the Table

While fintechs dominate design and engagement, banks remain the cornerstone of credibility and stability.

Their value in co-brand innovation lies in:

- Regulatory Strength: Deep understanding of compliance, AML, and customer protection.

- Balance Sheet Power: Ability to underwrite and absorb risk at scale.

- Operational Maturity: Infrastructure that ensures reliability, reconciliation, and dispute resolution.

- Trust Capital: The reassurance customers still associate with licensed institutions.

The most successful partnerships recognize this complementarity: fintechs innovate at the edge; banks anchor at the core.

Challenges on the Road to Scalable Co-Brand Innovation

Despite the momentum, several friction points continue to limit scale and sustainability:

- Regulatory Oversight: RBI’s evolving view on digital lending and BaaS models means co-brands must embed transparent risk governance early.

- Data Boundaries: Clear consent and auditability under the Digital Personal Data Protection Act, 2023 are critical for customer trust.

- Integration Fatigue: Many banks still run legacy core systems that slow down real-time API performance.

- Customer Clarity: Users often confuse roles who is responsible when an issue arises, the fintech or the bank?

Addressing these requires a partnership governance blueprint that defines roles, data-sharing policies, and escalation structures upfront.

The Road Ahead: Co-Branding as a Platform Strategy

The next phase of India’s co-brand evolution will be shaped by four drivers:

- Open Data Ecosystems: Account Aggregator and Public Credit Registry infrastructure will power hyper-personalized co-brands.

- AI-Led Personalization: Banks and fintechs will jointly deploy AI to tailor offers in real time based on contextual behavior.

- Embedded Finance Expansion: From travel to health to education platforms ,finance will integrate deeper across ecosystems.

- The RBI’s 2025 digital-lending and digital-banking frameworks: signalling a shift toward regulation-by-design, where compliance is built into system architecture and oversight is principle-based.

Building ecosystems that are sustainable, compliant, and adaptive will be the victors, not the ones who move the fastest.

Strategic Imperative: Learning from Each Other

- Fintechs can teach banks how to listen more effectively, develop more quickly, and create customer-focused experiences.

- Fintechs may learn from banks how to manage regulations, scale responsibly, and safeguard consumer confidence.

- These lessons come together in co-brand innovation. It is the framework for the next ten years of financial inclusion and digital expansion, not only a link between the old and the new.