Table of Contents

Introduction

The Reserve Bank of India’s new Master Direction on Payment Aggregators, released on September 15, 2025, is best understood as a long-awaited reset. It brings together a patchwork of earlier circulars from 2020, 2021, and 2023 into one single framework. But more than consolidation, it is aimed at creating a durable, future-proof regulatory scaffolding for India’s payments industry.

Need for ‘the shuffle’

The earlier guidelines, issued in 2020 and subsequently in 2023, were innovative at that time. They created the first licensing regime for non-bank aggregators and set minimum capital and escrow requirements. But much has changed since then. Offline acceptance has surged, cross-border digital commerce has accelerated, and fintech players have multiplied. Online transactions have been on rapid growth led by massive traction on E-commerce, Q-Commerce. What was once a niche activity is now systemically critical.

This forced the RBI to confront risks that were not as visible five years ago; gaps in refund cycles, unclear oversight on cross-border flows, and under-capitalized aggregators sitting at the heart of large transaction volumes. The 2025 framework is therefore RBI’s attempt to close these gaps decisively.

The Great Unification: Bringing the Physical World Under the Regulatory Umbrella

One of the most striking aspects of the new framework is the recognition that payment aggregation isn’t monolithic. The RBI has formally separated it into three categories physical, online, and cross-border. This matters because the risks are very different; a face-to-face UPI or Card transaction at a Kirana store is not the same as an e-commerce checkout, which again is not the same as handling a merchant’s overseas payments. By drawing these boundaries, the regulator can now apply rules tailored to each model, whether it is physical verification of high-risk offline merchants or strict FEMA compliance for cross-border flows.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

- The Impact:

This unification will have far-reaching effects across the industry:

- For Physical PAs: The transition from being technology service providers to fully regulated financial intermediaries is a bigger one. These entities must now apply for RBI authorization by a strict deadline of December 31, 2025. This requires them to meet the stringent net-worth criteria of ₹15 crore at the time of application, rising to ₹25 crore by the end of the third financial year of authorization. They will also be subject to the same rigorous norms for governance, data security, risk management, and dispute resolution that have governed online PAs.

- For the Ecosystem: A level playing field is finally established. The regulatory arbitrage that may have existed between online and offline players is now gone.

- For Merchants and Consumers: This is an unambiguous win. Merchants using POS devices managed by a PAP will now have the same level of security, standardized settlement processes, and access to a formal grievance redressal mechanism as e-commerce merchants. This builds immense trust and confidence at the grassroots level, assuring a small shop owner in a Tier-3 city that the digital payment ecosystem has their back.

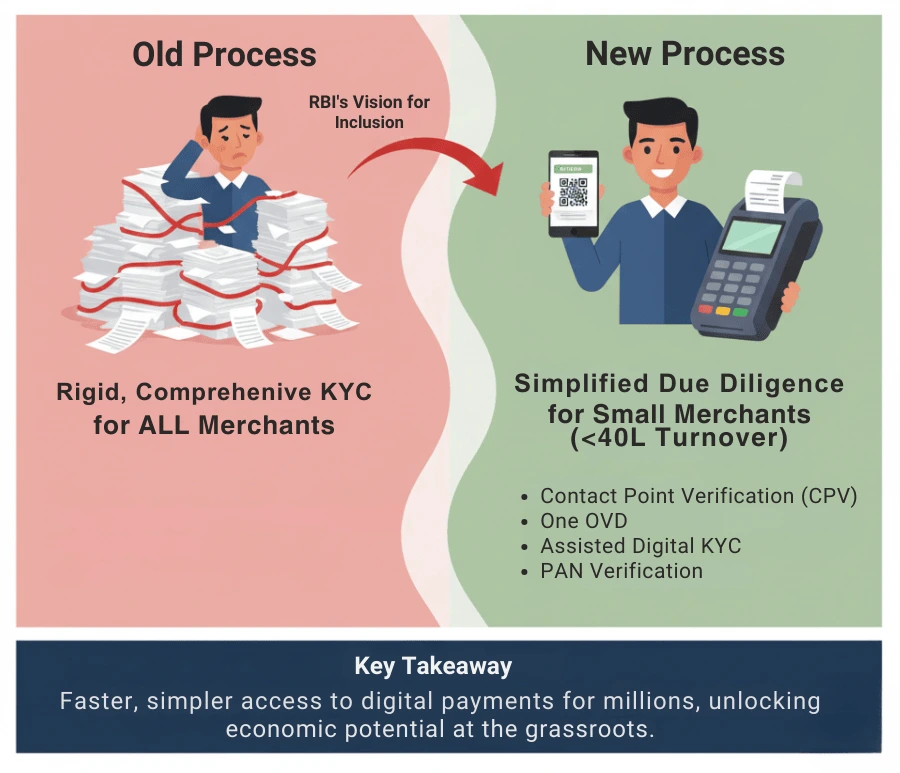

A Pragmatic Handshake with Small Merchants: Reimagining Due Diligence

While expanding its reach, the RBI has also shown remarkable pragmatism by acknowledging that a one-size-fits-all approach can stifle growth, especially at the smaller end of the merchant spectrum.

- The Old Hurdle

The previous guidelines mandated that PAs adhere to the RBI’s comprehensive “Know Your Customer (KYC) Master Direction” for all onboarded merchants. While essential for security, the full scope of these requirements could be intensive and time-consuming for small businesses and sole proprietors, creating a significant barrier to entry into the digital economy.

- The New Flexibility

- Verifying the merchant’s PAN from the issuing authority.

- Conducting a Contact Point Verification (CPV) of their place of business.

- Obtaining a certified copy of one Officially Valid Document (OVD) of the proprietor or authorized signatory.

Furthermore, the guidelines explicitly permit the use of “assisted modes” such as Digital KYC and agent-assisted Video-based Customer Identification Procedure (V-CIP), empowering PAs to use technology and field networks to onboard merchants efficiently.

A Dedicated Rulebook for Global Commerce and Evolved Fund Management

The RBI has gone further in segregating funds, explicitly prohibiting the netting of funds between inward and outward collection accounts. This means PAs cannot offset incoming and outgoing cross-border payment balances, requiring separate handling of these fund flows to enhance transparency and risk control.

Who gains? Who adjusts?

For banks, the framework formalizes their role as custodians of escrow and cross-border collection accounts. They will need stronger monitoring systems but also gain greater influence in the value chain.

For fintech aggregators, the immediate reality is higher compliance costs and operational overheads. Smaller players may pivot to becoming pure gateways (tech-only) or partner with banks rather than operating independently.

For merchants, the journey may become slower at the start, with more documentation and CPV checks. But in return, they will see faster refunds, predictable settlement, and consumer trust benefits that outweigh the initial friction.

And for consumers, the new regime offers what matters most; security, transparency, and faster grievance redressal.

Verdict

This RBI’s Master Direction achieves the difficult balance of tightening controls where systemic risk is a concern (such as in cross-border flows and capital adequacy) while simultaneously introducing flexibility where it can foster growth and inclusion (as seen with small merchant onboarding and settlement terms).

By consolidating rules, tightening weak spots, and future-proofing for offline and cross-border scenarios, the regulator has effectively drawn a line under the “wild west” phase of digital payments in India.

In the short run, compliance budgets might balloon, smaller players might exit, and onboarding might slow down. But over the medium to long term, as the ecosystem matures, consumers will gain confidence, and payments innovation will rest on firmer grounds.