Table of Contents

Introduction

In India, financial inclusion is not just a policy choice, it is a basic requirement for people to live with dignity, stability, and opportunity. Even today, in many Tier-2 and Tier-3 towns, families struggle to access essential financial services. Something as fundamental as a savings account, a safe credit option, or an affordable insurance or pension product is still out of reach for many. Access to mutual funds, quality lending, or even reliable merchant acceptance infrastructure continues to be uneven.

To address these gaps and ensure that every Indian can participate meaningfully in the formal financial system, the National Strategy for Financial Inclusion (NSFI) was crafted. It is a collective effort led by the Reserve Bank of India, working closely with institutions such as SEBI, IRDAI, PFRDA, NABARD, NSDC and others to strengthen and deepen India’s financial inclusion ecosystem for the economic wellbeing of people.

Building on the progress made under NSFI 2019–24, the RBI has now released NSFI 2025–30 to drive the next phase of inclusion, ensuring that financial services genuinely enhance the quality of people’s lives.

NSFI 2019–24: The Foundation for India’s Inclusion Journey

NSFI 2019–24 was built around a simple idea, too many people in India still found it difficult to use basic financial services. Whether it was opening a bank account, saving regularly, taking a loan, or even buying insurance, the process felt complex and out of reach for many households.

The strategy tried to break these barriers. Once people move to formal finance, they’re better protected, they avoid expensive informal lenders, and they’re able to handle emergencies with more confidence. It doesn’t just help the economy, it genuinely improves a family’s day-to-day stability.

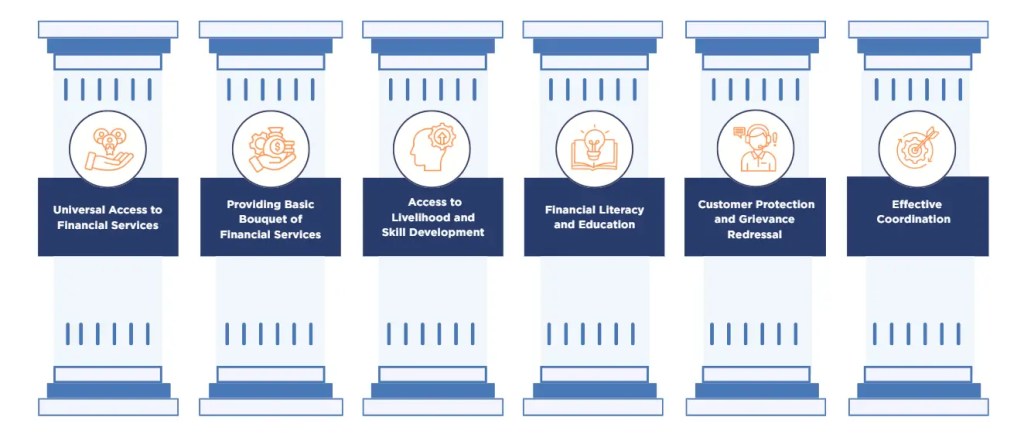

The strategy was built on six key pillars that focused on:

These pillars helped India move from isolated initiatives to a coordinated, nationwide inclusion framework.

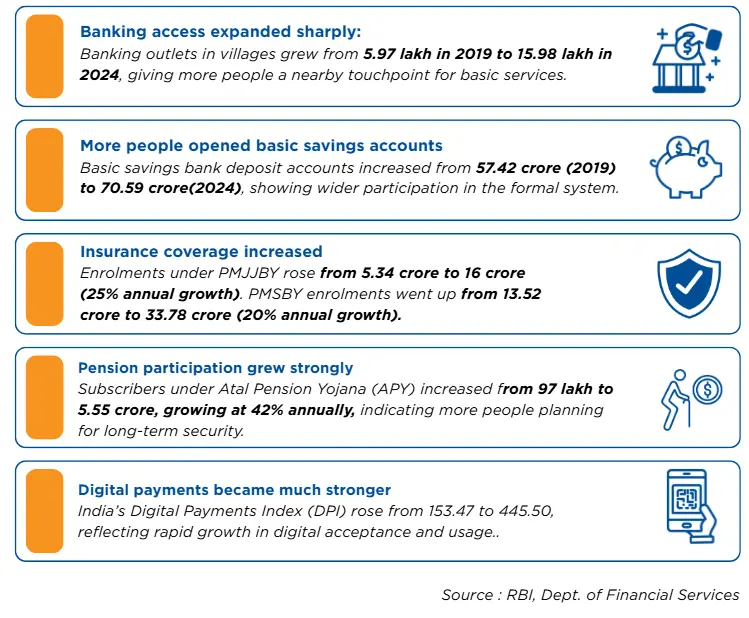

Across these pillars, the strategy defined some key milestones and delivered significant progress during the period 2019–24. Key outcomes included:

Why a New NSFI Was Needed

Even with these achievements, the ground reality showed that the job was far from complete.

- Supply-side gaps persisted: The last-mile network especially Business Correspondents was inconsistent. Many outlets were inactive, offered limited services, or provided an uneven customer experience. So, while access technically existed, it wasn’t always reliable.

- Demand-side barriers were even deeper: Many people had bank accounts but did not use them regularly. Income instability, lack of awareness, difficulty accessing credit, and low understanding of insurance and pension products kept people from engaging meaningfully. Women, particularly in rural regions, continued to face social and informational barriers.

- Service quality also held people back: Long queues, unclear grievance processes, and fear of digital transactions created hesitation especially among customers with low literacy or limited digital exposure.

All of this revealed a simple truth: India had largely solved the access problem, but not the usage problem and certainly not the trust problem.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

The Vision Behind NSFI 2025-30

The vision of NSFI 2025-30 is straightforward: to build a financial system that genuinely supports people’s wellbeing. The new strategy wants every Indian to receive financial services that are fair, affordable, easy to understand, and suited to their needs. It also recognises that financial services alone are not enough people need the right support system around them.

At its heart, the strategy links financial inclusion with real-life outcomes. It focuses on helping households achieve:

- Financial safety for day-to-day stability,

- Financial security through savings and insurance,

- Financial resilience to handle emergencies, and

- Financial discipline to build long-term habits.

When these four elements come together, financial services move beyond transactions – they become tools for a better, more stable life.

Introducing Panch Jyoti: Five Guiding Lights for India’s FI Journey

The centrepiece of NSFI 2025–30 is Panch Jyoti, a set of five strategic objectives that illuminate the next phase of India’s inclusion journey.

1. Improving the availability and use of Financial Services

The strategy emphasises expanding access to the full spectrum of savings, payments, remittances, insurance, credit, and pension products while ensuring they remain suitable and responsible. Affordability of essential services is positioned as a foundational right.

2. Gender-Sensitive, Women-Led Financial Inclusion

Women remain central to the India growth story, yet they face persistent gaps in access and usage. NSFI calls for differentiated credit models, targeted literacy, and resilience-building measures tailored to women and vulnerable households.

3. Linking Livelihoods, Skilling, and Market Access with FI

This is perhaps the biggest philosophical shift. Inclusion cannot succeed if income sources remain unstable. NSFI explicitly integrates livelihood organisations, skill-development networks, and market enablers into the FI framework.

4. Financial Education as a Tool for Discipline

The strategy moves education from sporadic campaigns to behavioural transformation encouraging households to save regularly, diversify investments, borrow responsibly, and plan for future life events.

5. Strengthening Consumer Protection and Grievance Redressal

Trust is the backbone of sustained financial usage. NSFI pushes for faster, more reliable grievance processes, improved awareness of rights, and a stronger safety net for customers navigating an increasingly digital ecosystem.

NSFI 2025-30 is India’s attempt to move from inclusion to empowerment from access to outcomes.

It reinforces that the next decade of financial inclusion will not be defined by how many people enter the system, but by how meaningfully the system supports their wellbeing.

What Banks and NBFCs Need to Reflect On

NSFI 2025–30 places financial institutions at the centre of India’s next inclusion leap. For banks and NBFCs, this is a reminder that real impact will come not just from opening more accounts, but from building services that people can trust, understand, and use with confidence.

Institutions will need to rethink how they design products for low-income households, how they simplify digital journeys, and how they educate and protect customers at every step.

As the strategy shifts the focus from access to outcomes, financial institutions must gear up for a future where quality of service, suitability of products, and resilience of customers become the true measures of inclusion. Those who adapt early with better data insights, stronger last-mile engagement, and more thoughtful customer support will be best positioned to lead India’s next chapter of inclusive growth.