Table of Contents

Systemic Challenges in MSME Credit Access

Micro, Small, and Medium Enterprises (MSMEs) account for roughly 30% of India’s GDP, contribute about half of total exports, and employ more than 110 million people. This scale is well documented yet, systemic frictions continue to constrain the sector’s growth. Persistent issues such as delayed receivables, restricted market access, limited adoption of digital tools, and heavy compliance costs remain key structural challenges.

Among these, the credit gap is the most binding constraint. Multiple studies, including those by SIDBI and MoMSME, confirm that a large share of MSMEs remain outside formal credit channels despite being operationally viable. The underlying reasons are clear and recurring: inadequate collateral coverage, inconsistent or informal bookkeeping, fragmented cash flows, and legacy underwriting models designed for asset-backed, large-enterprise lending.

While digital data sources (GST, UPI, e-invoicing, etc.) and policy initiatives have improved visibility, creditworthiness translation mechanisms have not evolved proportionally. As a result, MSME lending remains dependent on policy interventions rather than market-driven product innovation, leaving a sector critical to India’s growth still underserved by formal finance.

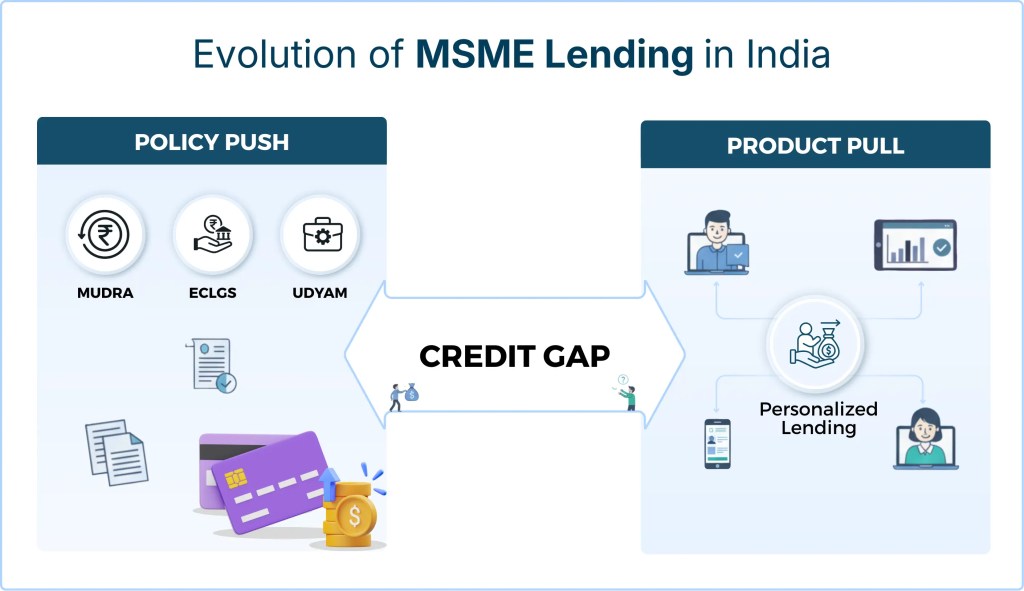

A Policy-Led Push, Not a Market-Led Pull

Over the past decade, government interventions from Mudra and ECLGS schemes to the Udyam registration framework have accelerated formalization and expanded visibility into the MSME ecosystem. However, while these policies have helped bring enterprises into formal finance, the approach has remained largely policy-push rather than market-pull. Credit continues to flow through standardized products designed around mandates instead of the lived realities of small businesses. As a result, the MSME credit gap estimated at approx ₹30 lakh crore still persists, highlighting the need for a shift from policy-driven inclusion to design-led lending innovation.

India’s MSME Credit Pain Points

For banks and NBFCs, the persistent MSME credit gap is less a question of intent and more one of economic and operational feasibility. Current credit models were built around collateral requirements, audited financial statements, and standardized risk parameters, frameworks originally designed for large, asset-heavy enterprises.

Most micro and small businesses operate outside these parameters. Their financial data is inconsistent, real-time performance visibility is limited, and origination costs per loan remain disproportionately high. Even with the increasing availability of digital data sources such as GST filings, UPI transaction trails, and e-invoicing, lenders struggle to translate raw data into reliable, actionable credit insights.

Consequently, lending processes remain optimized for regulatory compliance and risk protection, rather than for customer-centric product design. Addressing this misalignment requires rethinking lending as a design problem, where credit offerings are developed around actual MSME business models, cash-flow patterns, and behavioral data enabling products that are understood, valued, and actively demanded by small enterprises.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

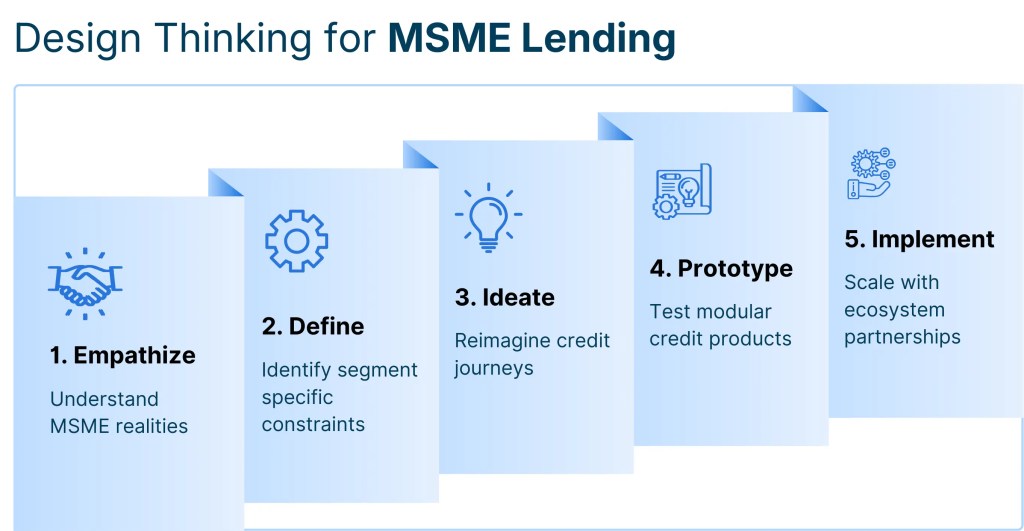

Bridging the MSME credit gap requires more than policy incentives it needs a paradigm shift in how these lending products were imagined, built, and delivered. This is where Design Thinking becomes a powerful enabler. Design Thinking reframes lending from a complex process to a co-creation journey, where solutions are built around empathy, context, and experimentation. By understanding each segment’s real constraints and motivations, lenders can design products that MSMEs pull rather than need to be pushed. For instance:

- A seasonal apparel manufacturer in Tiruppur may need flexible working capital limits tied to production and sales cycles, instead of fixed monthly repayments.

- A small logistics operator in Nagpur benefits from vehicle-linked credit with built-in maintenance buffers and variable EMIs based on fleet utilization.

- A digital services startup in Jaipur values revenue-based financing, where repayments flex with inflows, avoiding cash strain in slower months.

For lenders, such design-led lending not only improves adoption and asset quality but also deepens insight into borrower behavior, enabling smarter, data-driven portfolio management.

Reimagining MSME Credit: What Banks and NBFCs Can Do Next

For financial institutions, the path forward is in moving from standardized credit delivery to ecosystem-enabled value creation. By embedding design thinking into strategy and execution, banks and NBFCs can unlock new levers of growth and risk resilience. This means:

- Embedding Ecosystem Linkages into MSME Financing Models: Integrate credit products with MSMEs’ operating environments such as e-commerce platforms, agri-marketplaces, or manufacturing clusters to create contextual, data-backed lending opportunities. Ecosystem linkages enhance visibility, reduce origination costs, and build trust through anchored partnerships.

- Creating Customized Credit Solutions for Sector-Specific Needs: Move beyond generic term loans to design modular financial products tuned to industry realities from inventory-linked financing for retailers to milestone-based disbursals for small manufacturers. This ensures credit solutions resonate with how each sector earns, spends, and scales.

- Strengthening Risk Frameworks via Supply Chain Visibility: Leverage transactional and logistics data from upstream and downstream partners to develop network-aware risk models. Such models can anticipate stress early, reward resilient MSMEs, and enable dynamic pricing that reflects true business health.

- Driving Inclusive MSME Growth with Value Chain–Aligned Products: Develop holistic offerings that go beyond credit embedding payments, insurance, and advisory into the MSME’s value chain. This not only drives financial inclusion but also builds long-term relationships rooted in shared growth.

India’s MSME sector cannot progress on the basis of policy interventions and incremental lending schemes alone. The next phase of growth depends on the operational diversity and cash-flow characteristics of small businesses. This requires financial institutions to integrate data-driven assessment with human-centered product design.

Institutions that adopt this mindset will be better positioned to build financial products that MSMEs can easily understand, use effectively, and see value in moving from eligibility-based lending to solutions that align with how MSMEs actually operate.

Source: Annual Report 2022–23,” Ministry of Micro, Small and Medium Enterprises (MoMSME)

SIDBI: Understanding Indian MSME (13th May 2025)