Table of Contents

Introduction

Loans Against Securities have historically been positioned as a discreet, low-risk, high-margin product. It was built mainly for affluent customers those with large equity and mutual fund portfolios and predictable liquidity needs. That positioning no longer fits how LAS works today.

The spread of digital trading platforms, real-time demat integrations, API-based pledge mechanisms, and consumer investment apps has changed the nature of LAS. What was once a relationship-managed wealth product is now capable of operating as real-time, on-demand credit.

In this form, LAS can play a much larger role. It can support retail spending without unsecured risk, provide working capital to MSMEs without stressing cash flows, and sit directly inside digital platforms as an embedded credit option.

Yet most banks and NBFCs still look at LAS through an old lens. Product teams treat it as a niche offering. Risk teams handle it as a special case. Distribution still assumes branch-led, high-touch journeys.

This gap between what LAS can do and how it is currently treated is where the real opportunity lies.

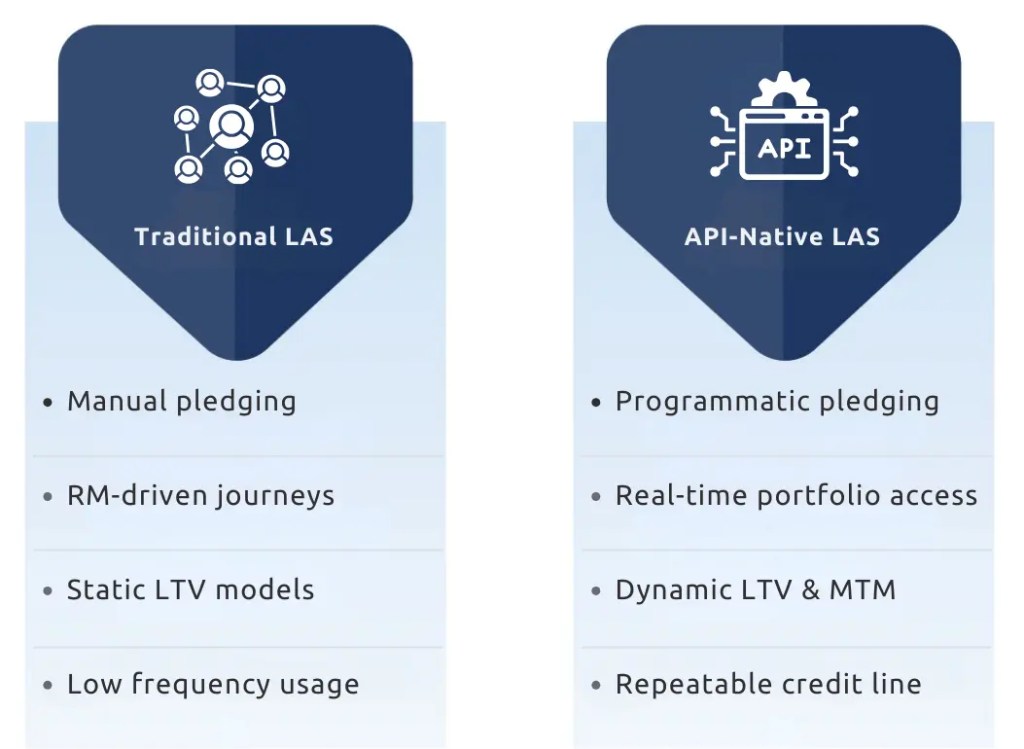

The Unlock: From Branch-Centric Pledging to API-Native LAS

Traditional LAS was never designed to scale. The process was slow and manual. Pledging required paperwork, approvals took days, and risk checks were infrequent and static. Digital wealth platforms have quietly changed this. Today, equities, mutual funds, and even bonds can be pledged and monitored digitally.

Two changes stand out.

- First, lenders can see portfolios in real time. Broker and RTA integrations allow continuous visibility into holdings and values.

- Second, risk controls can run automatically. LTV limits, margin checks, top-ups, and liquidation rules no longer depend on manual review. They can respond to market movements as they happen.

Because of this, LAS is shifting from a specialised loan product to something closer to embedded credit infrastructure.

Why LAS Fits Embedded Credit Better Than Personal Loans or BNPL

Most embedded credit today is unsecured. Personal loans and BNPL rely on bureau data, spending patterns, and behavioural signals. These models scale quickly, but they are fragile. Customer acquisition is expensive, defaults can spike, and lenders are forced to compensate with higher pricing or tighter terms.

LAS works differently. Instead of lending based on behaviour, it is backed by assets that already exist and can be valued continuously. The following changes the economics:

- First, the risk is lower. Because the loan is secured, losses and capital requirements are lower. This allows competitive pricing even for smaller or short-term use cases.

- Second, risk is managed continuously. LTV monitoring and mark-to-market checks happen automatically, without operational friction.

- Third, usage is flexible. Once a portfolio is pledged, customers can draw, repay, and redraw as needed. It behaves more like a credit line than a one-time loan.

Where Embedded LAS Actually Comes Alive

Future growth in LAS is unlikely to come from adding more wealthy customers. It will come from new use cases where portfolios already exist, but liquidity is limited.

- Investment apps

Retail investors today build steady portfolios through SIPs, mutual funds, and ETFs. These portfolios are diversified and grow over time. Investment apps can turn them into simple credit lines, giving users access to liquidity without selling investments. For users, this feels practical and familiar, not like taking a loan. - MSME platforms

Many MSMEs hold demat assets as promoter investments or treasury holdings, but still rely on unsecured loans for working capital. LAS allows them to borrow against existing assets, top up when needed, and avoid pressure on business cash flows. For B2B platforms, this can be a simpler and safer lending option.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

- Digital bonds and government securities

As bonds and treasury products become digital, investors increasingly want liquidity without breaking long-term positions. LAS enables short-term credit against these assets, often with better outcomes than early redemption. - Retail marketplaces

Embedded credit is common at checkout, but mostly unsecured. LAS introduces another option. Customers can pledge investments, access lower-cost credit for larger purchases, and repay over time. This opens the door to portfolio-backed consumer credit.

Across all these examples, the pattern is the same. When portfolios become usable in real time, LAS stops looking niche and starts behaving like infrastructure.

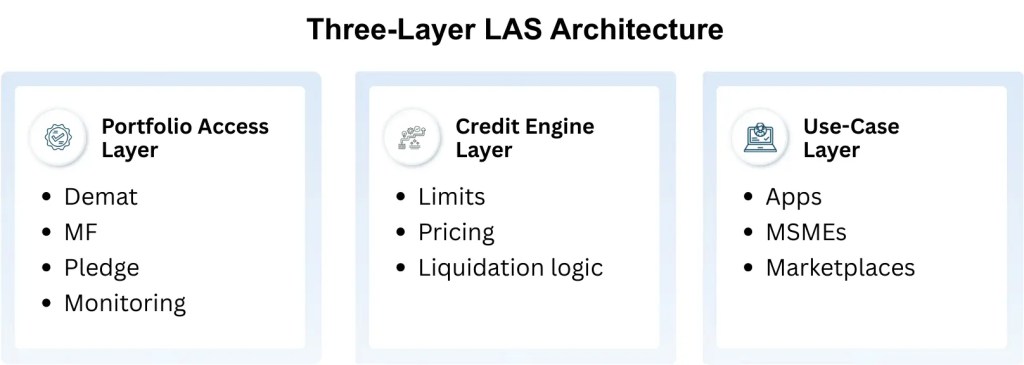

A Strategic Framework: LAS as a Three-Layer Embedded System

Reframing LAS for the Next Decade: A Three-Layer View

Instead of viewing LAS as a single product, it helps to think of it in layers.

Layer 1: Portfolio Access

This is the foundational layer demat and mutual fund connectivity, pledge creation, real-time valuation, and monitoring. Most institutions already operate here. The focus is largely operational: access, custody, and compliance.

Layer 2: Credit Engine

This is where differentiation begins. Dynamic LTV frameworks, exposure management across asset classes, intraday risk controls, and pricing models that respond to volatility rather than static slabs. Very few players truly own this layer today; many outsource or oversimplify it.

Layer 3: Use-Case Layer

This is where LAS becomes embedded. Consumer investment apps, MSME platforms, retail marketplaces, broker ecosystems—each requires LAS to be abstracted into seamless journeys rather than standalone loans.

Most incumbents remain confined to Layer 1. The strategic opportunity lies in deliberately building ownership of Layer 2 and selectively orchestrating Layer 3.

The Larger Shift

Unsecured embedded credit is starting to show its limits. At the same time, more individuals and businesses in India are holding financial assets than ever before. LAS sits at the intersection of these two trends.

What was once a quiet wealth product is becoming a practical, scalable way to offer secured credit inside digital platforms. The institutions that succeed will not treat LAS as a side offering. They will build it as core infrastructure.