Table of Contents

A Structural Shift in How Value Is Being Created

For much of the past decade, fintech innovation was synonymous with consumer disruption – neobanks, wallets, BNPL products, and elegant front-end experiences. This wave succeeded in driving adoption, but it also exposed fundamental limits: rising customer acquisition costs, fragile unit economics, regulatory sensitivity, and limited long-term defensibility. Today, global investor capital is moving decisively away from surface-level innovation and toward a deeper, more consequential layer of the financial ecosystem: enterprise fintech. This is not a cyclical correction. It reflects a structural reassessment of where financial value is created, protected, and compounded.

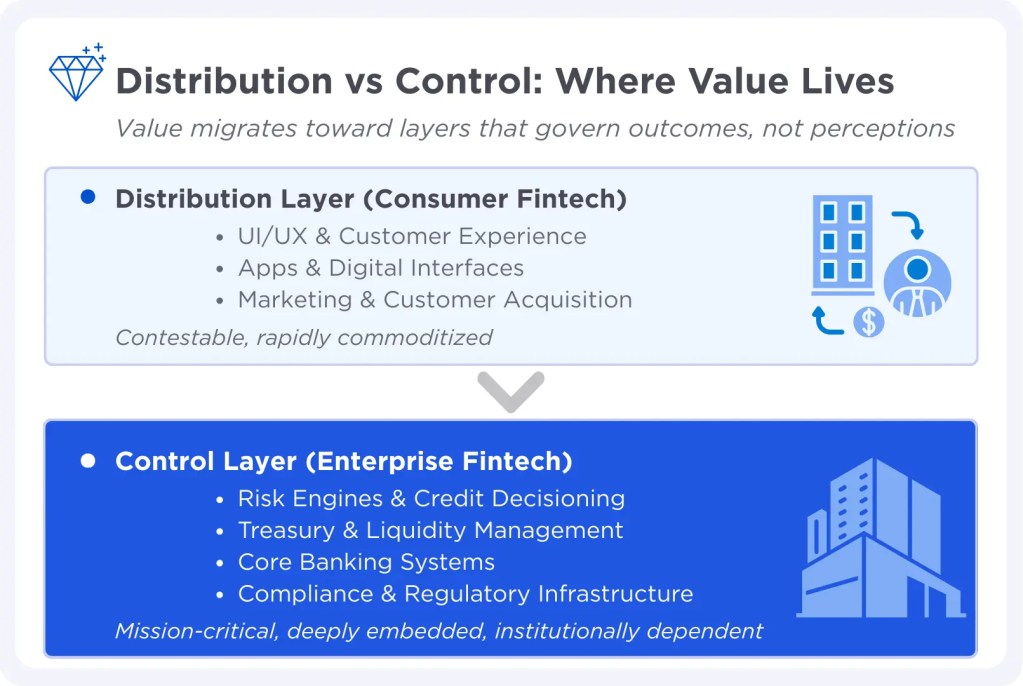

From Distribution to Control: The New Centre of Gravity

Consumer fintech optimised distribution interfaces, branding, and reach. Enterprise fintech governs control how capital is allocated, how risk is priced, how liquidity is managed, and how regulatory truth is produced. Platforms embedded at these control points influence credit approvals, intraday liquidity decisions, continuous risk recalibration, and automated regulatory reporting. Once deployed at this layer, enterprise fintech solutions stop behaving like vendors and begin functioning as institutional infrastructure.

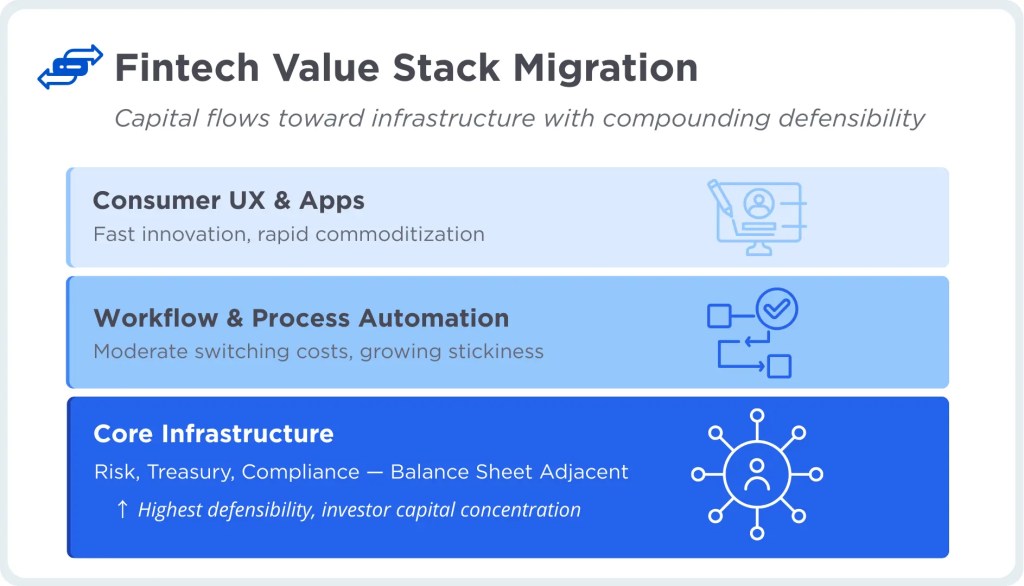

The Fintech Value Stack Is Migrating to Core Systems

Early fintech innovation focused on onboarding flows and user journeys. These drove adoption but commoditized rapidly. As a result, investor capital has systematically migrated down the fintech value stack toward layers where economics compound over time. This migration is most visible in:

- Core banking and lending modernisation

- Treasury and liquidity management platforms

- Payments orchestration and reconciliation layers

- RegTech and compliance automation

- Embedded data and AI decision engines

These platforms are deeply integrated, a very critical part of the ecosystem, and regulator-facing. Replacing them can disrupt operations and can be institutionally risky.

Why Enterprise Fintech Has Structurally Superior Economics

Enterprise fintech platforms are not transactional products; they are critical financial infrastructure, and their economics reflect this reality. They are characterised by:

- Long-term contracts (3–7 years): Institutions commit for multiple years because implementation takes time, requires approvals, and switching creates operational risk leading to stable, predictable revenue.

- Deep integration into core systems: These platforms plug into core banking, ERPs, and daily workflows. That makes them hard to replace and increases customer stickiness.

- Regulatory dependency: Meeting regulatory requirements is central to the product, which creates strong barriers for new entrants.

- Expansion-led growth: Customers often start with one module and add more over time, which drives strong retention and account growth.

Growth is driven not by customer acquisition, but by integration depth, usage expansion, and institutional reliance.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

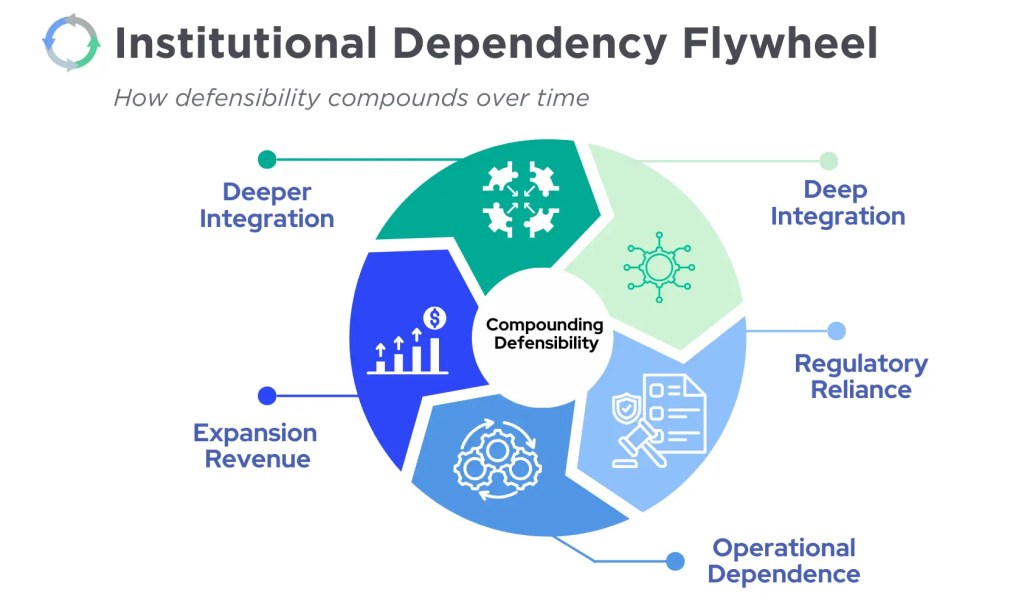

Defensibility Reimagined: Institutional Dependency

While Enterprise fintech creates a fundamentally stronger form of defensibility than traditional SaaS. Competitive advantage emerges not from features alone, but from institutional dependency.

- Platform outputs shape balance-sheet decisions, directly influencing credit, liquidity, and capital allocation.

- Risk and compliance teams rely on embedded system intelligence for monitoring, reporting, and regulatory adherence.

- Regulators become familiar with and implicitly trust platform workflows, reducing appetite for system change.

- Internal teams develop operational muscle memory, embedding the platform into day-to-day decision-making and processes.

At this point, displacement risk becomes asymmetrical. Replacing the platform introduces regulatory, operational, and financial risk that far outweighs any incremental improvement a competitor may offer. provides

From AI Adoption to Measurable Financial Outcomes

AI adoption in enterprise fintech has moved beyond experimentation. Leading financial institutions are now deploying AI where it directly impacts balance-sheet efficiency, risk management, and operating economics. Value is emerging across three core clusters:

- Risk, credit, and fraud, through continuous portfolio monitoring and early stress detection

- Compliance and controls, through automated regulatory interpretation and embedded monitoring

- Liquidity and operations, through predictive cash-flow forecasting and operational risk intelligence

Collectively, these capabilities lower cost-to-serve, improve capital efficiency, and raise risk-adjusted returns. AI is no longer a feature – it is becoming embedded financial intelligence.

India: A Strategic Inflection Point for Enterprise Fintech

India stands out as one of the most important enterprise fintech markets globally- not only because of scale, but because of structural readiness.

Three forces converge uniquely in India:

1. Scale with Margin Sensitivity

Indian banks and NBFCs process billions of transactions annually, often at thin margins. Even small efficiency gains translate into outsized financial impact. A 10-basis-point improvement in cost-to-serve can mean hundreds of crores in annual savings.

2. Digital-First Regulatory Infrastructure

Platforms such as UPI, Account Aggregator, and digital KYC have created an API-driven regulatory environment that accelerates enterprise fintech adoption rather than slowing it. India may be the only major market where regulation enables innovation at this pace.

3. Legacy Systems Under Stress

Rapid balance-sheet growth layered on legacy cores has exposed limitations in risk management, treasury visibility, regulatory reporting, and data consistency. This creates strong demand for modular, cloud-native enterprise fintech platforms.

For global investors, India is increasingly seen as both a large-scale market opportunity and a live laboratory for enterprise-grade financial innovation. Solutions proven in India’s high-volume, low-margin environment can be exported to markets facing similar challenges.

What This Means for CXOs, Boards - and the Industry

Enterprise fintech is no longer an IT modernisation initiative. It is a strategic capability with direct implications for valuation, resilience, and competitiveness. Technology decisions are increasingly capital allocation decisions, with long-term balance-sheet consequences. Leadership teams must now ask where inefficiencies silently erode margins, which systems constrain scale or regulatory confidence, and how returns on technology investments should be measured in strategic – not merely operational – terms.