Fintech partnerships are accelerating growth but increasing risk. Learn how banks and NBFCs can manage governance, compliance, and digital lending...

Know moreFostering Successful Bank-Fintech Partnerships with a Robust Governance Framework

The rapid evolution of the fintech Industry has fundamentally transformed the financial services landscape. Traditional banks, seeking to remain competitive and innovative, are increasingly partnering with fintech companies to enhance their service offerings, streamline operations, and deliver superior customer experiences. However, the success of these collaborations hinges on establishing a robust governance framework. This article explores the

- Construct of bank-fintech partnerships

- Critical considerations from product and business perspectives

- The need for a program management approach,

- Designing an effective governance framework

- How Bank-Fintech Partnerships are Changing the Ecosystem

Before the rise of fintech partnerships. Traditional banking systems were often bogged down by outdated technologies, leading to operational inefficiencies and a slow response to customer needs. The rapid evolution of the fintech industry has transformed the financial services landscape. Traditional banks are increasingly partnering with fintech companies to enhance service offerings, streamline operations, and deliver superior customer experiences. The success of these collaborations hinges on establishing a robust governance framework.

However, the advent of fintech partnerships has dramatically transformed the landscape in the following ways:

- Accelerated Digital Transformation: Accelerated transformation allows banks to keep pace with technological advancements and meet the evolving expectations of tech-savvy customers. For instance, collaborations have enabled banks to offer mobile payments, digital wallets, and online investment platforms

- Risk Management and Compliance: Fintechs provide cutting-edge tools for fraud detection, risk assessment, and regulatory compliance. This can help banks mitigate risks and ensure adherence to regulatory requirements.

- Innovation Acceleration: Agile development and rapid deployment of new technologies meet market demands efficiently. Fintechs’ innovative approaches have enabled banks to quickly develop and launch new products and services, such as personalized financial advice services and integrated payment solutions.

- Enhanced Customer Experience: Fintechs offer seamless, user-friendly digital solutions, improving customer engagement and satisfaction. This can lead to higher customer retention and loyalty.

- Access to New Markets: Banks gain entry into niche markets and expand their customer base through specialized approaches. Fintechs often have innovative solutions that cater to specific customer segments, such as millennials or small businesses.

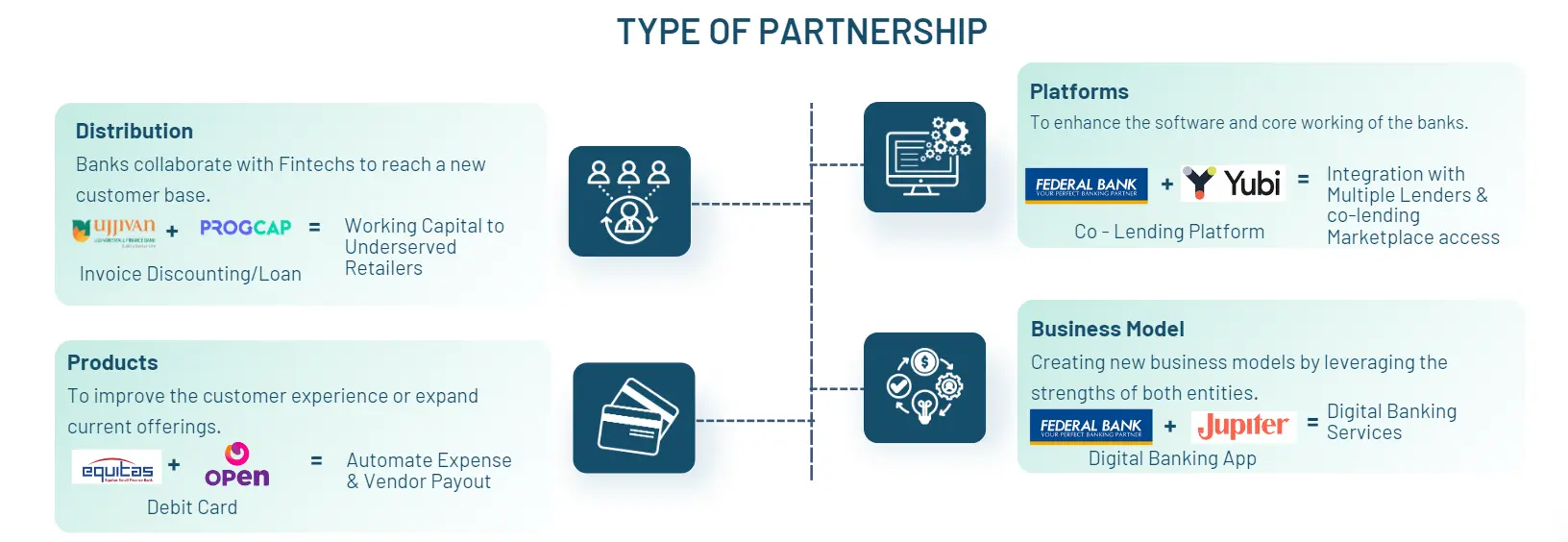

Understanding the Bank-Fintech Partnerships

Bank-fintech partnerships can take on various forms, each designed to leverage the strengths of both entities:

- Business Model Partnerships: Creating new business models by leveraging the strengths of both entities. For example, credit line facilities through mobile apps cater to the evolving needs of consumer credit, offering flexible and instant access to funds.

- Platform Partnerships: Enhancing software and core banking functions through integration. Collaborative efforts have resulted in advanced digital banking services, such as mobile banking apps and digital wallets, WhatsApp banking, etc.

- Distribution Partnerships: Reaching new customer bases through innovative distribution channels. Services offered through merchant networks have expanded the reach of financial products like loans, FD insurance, etc.

- Product Partnerships: Enhancing customer experience or expanding product offerings through joint development like Co-branded credit cards offering personalized financial services and integrated payment solutions.

Trends in Bank Fintech Partnership

- SME Financing: Specialized products focusing on small and medium enterprises (SMEs) have been developed, offering tailored loans that consider the unique challenges and cash flow cycles of SMEs.

- Secured Lending: Many SME loans are secured against business assets, inventory, or receivables, with fintech platforms providing improved monitoring and data analytics for risk management. Digital documentation further simplifies the process, reducing risks for banks and enhancing accessibility for borrowers.

- Open Banking: The rise of open banking has allowed for greater interoperability between banks and fintechs. By leveraging open APIs, banks can offer a range of third-party services, creating a more comprehensive financial ecosystem for customers.

- Digital Onboarding: Streamlined digital onboarding processes have reduced the friction associated with opening new accounts. Banks can now offer quick and efficient digital account opening services, enhancing the customer acquisition process.

- Embedded Finance: The integration of financial services into non-financial platforms has become increasingly popular. Banks are partnering with fintechs to embed financial products within retail, travel, and other industries, providing customers with seamless access to financial services within their everyday activities.

Critical Considerations from a Product & Business Perspective

When approaching product development and business strategy, several critical considerations can significantly impact success. Here are some key aspects from both product and business perspectives:

Product Innovation and Development: Integrating fintechs’ intuitive and user-friendly designs into the bank’s product offerings to enhance customer satisfaction. This includes ensuring that digital interfaces are easy to use and accessible to a wide range of customers.

Integration and Interoperability: Using robust APIs to facilitate secure data exchange and functionality integration. APIs enable different systems to communicate effectively, ensuring seamless service delivery.

Business Alignment and Strategy: Both parties must have a clear, shared vision of the partnership’s goals. KPIs should be regularly reviewed and adjusted as needed to stay on track.

Need for Program Management Approach:

Coordinating Complex Initiatives: Efficiently coordinating various projects and initiatives is essential for managing the complexity of bank-fintech collaborations. Clear project timelines, roles, and responsibilities help ensure that projects stay on schedule and within budget.

Milestone Tracking: Monitoring progress against predefined milestones ensures that initiatives are on track. Regular tracking helps identify any deviations from the plan, allowing for timely corrective actions.

Resource Management: Optimal allocation and utilization of financial, technological, and human resources maximize efficiency and minimize waste. Effective resource management ensures that both parties can leverage their strengths to achieve mutual goals.

In bank-fintech partnerships, the governance framework is critical to ensure that both parties align strategically and operationally while complying with regulatory requirements and safeguarding stakeholder interests.

Types of Policies:

- Financial Regulations: Ensuring compliance with financial laws and standards prevents legal issues and maintains the integrity of financial operations.

- Data Protection: Safeguarding customer and transaction data through stringent data protection policies ensures the security and privacy of sensitive information.

- Consumer Rights: Protecting the rights and interests of consumers through comprehensive policies enhances trust and customer satisfaction.

Types of Contracts:

- Scope and Responsibilities: Clearly defining the duties and responsibilities of each party ensures clarity and prevents misunderstandings.

- Intellectual Property: Addressing ownership and usage rights of developed technologies and solutions safeguards the interests of both parties.

- Termination and Dispute Resolution: Establishing terms for contract termination and methods for resolving disputes provides a clear framework for managing potential conflicts.

Risk and Compliance Management:

- Cybersecurity Threats: Identifying and mitigating potential cybersecurity risks through regular assessments and updated security measures protects the partnership from cyber threats.

- Compliance Breaches: Ensuring adherence to regulatory requirements through robust compliance management practices prevents regulatory breaches and maintains operational integrity.

Partnership Management:

- Dedicated Teams: Establishing teams responsible for managing partnerships supports effective collaboration and decision-making.

- Clear Communication Channels: Facilitating effective communication between bank and fintech partners ensures seamless collaboration and quick issue resolution.

- Relation Management: Management of the stakeholders and working closely with the teams of the parties.

KPI Management:

- Setting Clear KPIs: Establishing measurable indicators for tracking partnership success helps both parties understand the effectiveness of their collaboration like Revenue tracking, seamless working of technology, customer satisfaction, etc.

- Regular Reviews: Periodically reviewing KPIs ensures that goals are met and allows for necessary adjustments to maintain alignment with partnership objectives. Having Partner Audits, operational Audits, creating proper review mechanisms and timelines, etc.

Conclusion

Bank-fintech partnerships drive innovation and growth in the financial industry. Achieving success requires a well-structured governance framework that addresses critical considerations from product and business perspectives and employs a robust program management approach. By focusing on these key areas, banks and fintechs can create synergistic collaborations that deliver enhanced value to customers and achieve sustainable success. Effective governance helps navigate the complexities of integration, maintain compliance, and deliver innovative solutions that meet the ever-evolving needs of the market. Through these efforts, bank-fintech collaborations can transform the financial services landscape, driving forward a new era of digital finance.

RELATED POSTS

Policy vs Practice: Why Most Compliance Failures Happen on the Ground

Most compliance failures aren’t policy issues - they’re execution gaps. Learn why compliance breaks on the ground and how to...

Know more

The Corporate Card Opportunity Nobody’s Talking About | The Next B2B Fintech Infrastructure Play

Corporate cards for SMEs could become the next major fintech infrastructure play. Explore how B2B cards, spend management platforms, and...

Know more