Table of Contents

Introduction

The Digital Personal Data Protection Act (DPDPA) marks a critical shift in India’s regulatory landscape as it directly impacts how financial institutions collect, store, process, and share personal data. For banks, NBFCs, cooperative institutions, and fintechs, this legislation is more than just a legal requirement, it introduces a structured accountability framework that demands visible and verifiable action across the entire data lifecycle.

As enforcement draws nearer, institutions must move beyond high-level awareness to concrete implementation. Consent mechanisms, purpose limitation, data deletion workflows, encryption, breach reporting, and third-party oversight are no longer optional, they are regulatory imperatives.

In this article, The Digital Fifth presents a clear, actionable roadmap that translates DPDPA’s principles into practical steps for compliance, backed by examples, tools, and industry-tested approaches. It outlines the five key pillars that institutions must focus on, covering regulatory mandates and implementation insights.

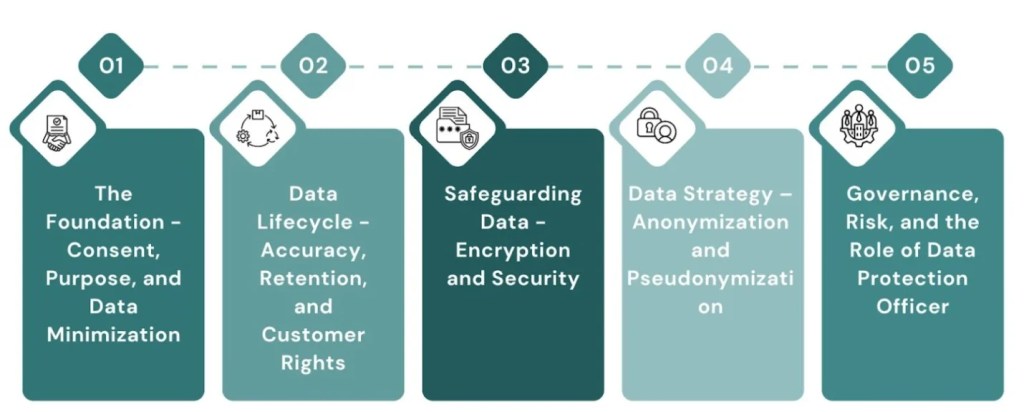

Five Pillars of Digital Personal Data Protection Act (DPDPA) Readiness for Financial Institutions

- 1. The Foundation - Consent, Purpose, and Data Minimization

At its core, DPDPA rests on the principle of data sovereignty—the idea that personal data belongs to the individual, not the institution collecting it. As such, every step in the data lifecycle now begins with explicit, informed, and revocable consent.

Breaking down the terminologies:

- Explicit: No pre-checked boxes or vague disclaimers.

- Informed: The customer must know what data is collected and why.

- Revocable: Withdrawal of consent should be as easy as giving it.

To give an example, if a bank collects a mobile number during savings account opening and takes consent to send OTPs, that’s acceptable. But sending product marketing messages on the same number later without fresh consent violates the DPDPA.

Another important clause of data minimization means collecting only what is necessary for the stated purpose. Asking for educational background during FD account creation, unless tied to a financial advisory service, is non-compliant.

Practical Measures:

- Create separate consent workflows for each use case: marketing, transactional alerts, and partner communications.

- Use granular checkboxes during onboarding, mapped to specific data elements (e.g., email for OTPs vs offers).

- Regularly review all data fields collected across channels and eliminate those with no valid purpose justification.

- 2. Data Lifecycle - Accuracy, Retention, and Customer Rights

The Act places significant emphasis on ensuring that data is not only collected properly but also updated accurately, retained appropriately, and deleted when no longer needed.

1. Talking about Accuracy first, many institutions still rely on batch processing for data updates, resulting in delays, mismatches, or missed communications. Consider a scenario where a customer updates their mobile number through the bank’s net banking platform. If this update is not reflected in the CRM, marketing, and notification systems in real time, the bank may send alerts to an outdated number, creating both a service failure and a compliance breach.

2. Next is Retention. DPDPA mandates that data must be stored only for as long as it serves its legal or business purpose. If a credit card application is rejected, associated data like bank statements or employment proofs must be automatically deleted within a defined retention period, unless legally required otherwise.

Customer Rights:

- Right to access their data.

- Right to correct inaccuracies.

- Right to request deletion when consent is withdrawn, or the purpose is fulfilled.

Operational Enhancements:

- Enable self-service correction portals in mobile banking apps.

- Integrate retention policies with auto-deletion workflows using tools like NetApp SnapLock or Securiti.ai.

- Log all consent revocation and deletion requests with audit trails to demonstrate compliance.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

- 3. Safeguarding Data - Encryption and Security

With digital threats becoming more sophisticated, DPDPA mandates end-to-end protection to ensure that data remains secure not just at rest, but also while being transferred and processed.

- Data at Rest: Stored data like scanned Aadhaar documents or transaction logs must be encrypted using industry-grade standards (e.g., AES-256). Banks using outdated algorithms or retaining backups in plain text face significant risks.

- Data in Motion: TLS 1.3 must be the baseline for secure communication. Whether it’s APIs between UPI and CBS, or CRM to contact center, encryption must extend across internal and external traffic.

- Data in Processing: This is about data that’s currently being used for scoring loans, verifying credentials, or detecting fraud. Techniques like homomorphic encryption now allow processing of encrypted data without ever decrypting it, which is ideal for outsourced analytics or AI models hosted on the cloud.

- Example Use Case: A bank uses encrypted transaction data to detect abnormal spending behavior through a third-party analytics engine. The service provider never sees raw customer information, yet delivers insights using secure processing.

Recommended Controls:

- Use Hardware Security Modules (HSMs) for key rotation and secure encryption.

- Mask personal identifiers (e.g., Aadhaar) in logs using dynamic tokenization.

- Encrypt data exports, backups, and report files, especially during file transfer to auditors or regulators.

- 4. Data Strategy – Anonymization and Pseudonymization

A well-structured data strategy under DPDPA requires institutions to rethink how personal data is handled, not just during collection, but across analytics, product testing, and external collaboration. Two critical techniques that enable this while reducing compliance risk are anonymization and pseudonymization.

Anonymization refers to the irreversible transformation of personal data so that an individual can no longer be identified, either directly or indirectly. Once data is anonymized, it falls outside the scope of DPDPA, making it ideal for use cases like:

- AI model training (e.g., fraud detection, loan default prediction)

- Product usage analytics

- Public data reporting (e.g., UPI heatmaps by region)

Pseudonymization, in contrast, replaces identifiable information with pseudonyms, such as random IDs, that can be re-linked to the original identity using a secure key. While still within the scope of DPDPA, pseudonymized data significantly reduces exposure risks and is well-suited for internal use cases where identity linkage might occasionally be required.

These approaches help banks decouple identity from behavior, enabling them to extract insights while limiting access to personal identifiers. Below are a few practical examples of how banks and fintechs are applying these techniques.

Banking Examples:

- A fraud risk team monitors suspicious patterns using masked data and only re-identifies the user for further action after risk scoring.

- A developer team uses anonymized transactional logs in UAT environments to simulate real-world scenarios without exposing customer PII.

Implementation Tips:

- Use enterprise-grade pseudonymization tools with secure key management.

- Replace production datasets with synthetic data for developer testing and model training environments.

- Enforce clear policies for controlled re-identification, with audit trails and role-based access logged via identity governance tools.

- 5. Governance, Risk, and the Role of the Data Protection Officer

Most financial institutions, including public and private sector banks, are expected to be categorized as a Significant Data Fiduciary (SDF). This status brings added obligations under the DPDPA.

Key Requirements:

- Appoint a Data Protection Officer (DPO) based in India, reporting to the board or the highest governing body.

- Maintain a Record of Processing Activities (RoPA) that documents how every category of data flows through your systems.

- Conduct Data Protection Impact Assessments (DPIAs) for new products or technologies that pose privacy risks.

- Ensure breach notification within 24 hours of becoming aware of any data compromise.

Strategic Considerations:

- DPDPA compliance must be seen as a business capability, not just a regulatory cost.

- Institutions with well-structured consent systems, deletion workflows, and risk monitoring will be better equipped for open banking, AI, and embedded finance ecosystems.

- Tools like OneTrust, MetricStream, ServiceNow GRC, and Splunk can automate audit trails, incident tracking, and DPIA reporting.

Preparing for Compliance Before the Clock Starts

With the DPDPA Rules, 2025 already released for public consultation and enforcement expected to begin in the next 6–8 months, financial institutions are entering a crucial preparation window. Once the rules are notified in the Official Gazette, timelines for setting up internal compliance frameworks, reporting mechanisms, and breach notification systems will come into effect, alongside the formal constitution of the Data Protection Board of India.

While the government is expected to offer a phased transition period of up to two years, this buffer should not be mistaken for a reason to delay. The nature of DPDPA compliance spanning consent management, data mapping, encryption, rights processing, breach response, and RoPA documentation requires thoughtful planning, cross-functional alignment, and execution readiness. Many institutions will need to overhaul legacy systems, re-architect customer journeys, and embed privacy-by-design principles into product lifecycles.