Table of Contents

In our previous edition, we explored the strategic underpinnings of the Digital Personal Data Protection Act (DPDPA) and its critical role in reshaping data governance across India’s digital financial ecosystem. As digital banking and embedded finance redefine how data is generated, shared, and used, the DPDPA introduces a much-needed framework that prioritizes customer rights, informed consent, and purpose-driven data usage.

The strategic imperative is clear as digital banking and embedded finance models have to redefine data generation, sharing, and usage patterns, organizations that master privacy-by-design will gain competitive advantage through enhanced customer trust and regulatory confidence.

However, strategic intent of DPDPA implementation from Financial Institutions must now translate into operational excellence. The evolving digital banking adoption from customers demands addressing three fundamental questions that will determine success or failure:

How can organizations implement robust third-party oversight?

What operational transformations are required across internal processes and partner ecosystems?

And critically, what governance frameworks will ensure compliance is embedded, not just enforced?

India’s banking, financial services, and insurance (BFSI) sector is in the midst of a landmark transformation. The DPDPA sets a new benchmark for data governance that aligns decisively with ongoing digital shifts characterized by open banking platforms, embedded finance solutions, and an increasing dependence on Technology Service Providers (TSPs). In this article we are tracing the essential journey from strategic principles to seamless operational execution, offering real-world BFSI insights on building trust, securing compliance, and fostering continuous innovation.

Open Banking to Open Data Economy - DPDPA Implications

The open data economy reshapes BFSI by enabling rapid data flows beyond institutional boundaries, driven by innovative TSP partners. For example, many financial journeys start with digital onboarding enabled by an eKYC platform that verifies identity while capturing explicit consent. The “consent” here is not a paper form but a series of digital checkpoints that must be traceable and revocable per DPDPA standards. Similarly, lending decisions increasingly depend on real-time analytics engines powered by third-party vendors who process transaction histories and payment behaviors.

These scenarios strengthen the thought that personal data rarely resides within a single institution. The customer’s data travels across a complex web of TSPs handling collection, processing, and storage. While such collaboration accelerates customer-centric product delivery like instant credit offers or personalized financial advice, it simultaneously expands the regulatory perimeter. The bank or insurer is responsible for every partner’s data practices, underscoring the urgent need to govern TSPs tightly. Some of the key Transformation Areas for the FInancial Institutions to focus, to ensure that the rights of the customers & the compliance requirements of DPDPA are met are:

- Consent-First Architecture: Open Banking 2.0 must embed DPDPA-compliant consent capture, purpose limitation, and seamless revocation across all user journeys, transforming how customer relationships are initiated and maintained.

- Enhanced Third-Party Governance: Technology Service Providers (TSPs) and DEPA intermediaries require stricter oversight frameworks, as data fiduciaries remain fully accountable for downstream data handling regardless of operational delegation.

- Precision Data Sharing: Bi-directional data exchange must be constrained to purpose-specific, disclosed activities, supporting DPDPA’s data minimization principles while enabling innovation.

- Transparent Product Development: Cashflow-based lending and embedded finance products must be architected with explicit, contextual consent mechanisms, creating more user-controlled experiences.

- Expanded Liability Framework: Data intermediaries face direct compliance scrutiny, making privacy-by-design essential across the entire ecosystem rather than optional.

Financial institutions that successfully navigate these transformations will become trusted stewards of data, gaining priority access to valuable customer insights while competitors struggle with compliance challenges.

The Central Role of TSPs in Open Banking 2.0

At the core of this evolution is the pivotal role of TSPs, acting as the connective tissue enabling secure, scalable, and innovative digital services. Open banking and embedded finance rely heavily on a dynamic network of TSPs handling functions like eKYC, analytics, cloud processing, and secure communications. Consequently, most personal data no longer lives within a single institution but moves fluidly through multi-party digital ecosystems.

Operationalizing DPDPA: Data Lifecycle Management Anchored by TSP Governance

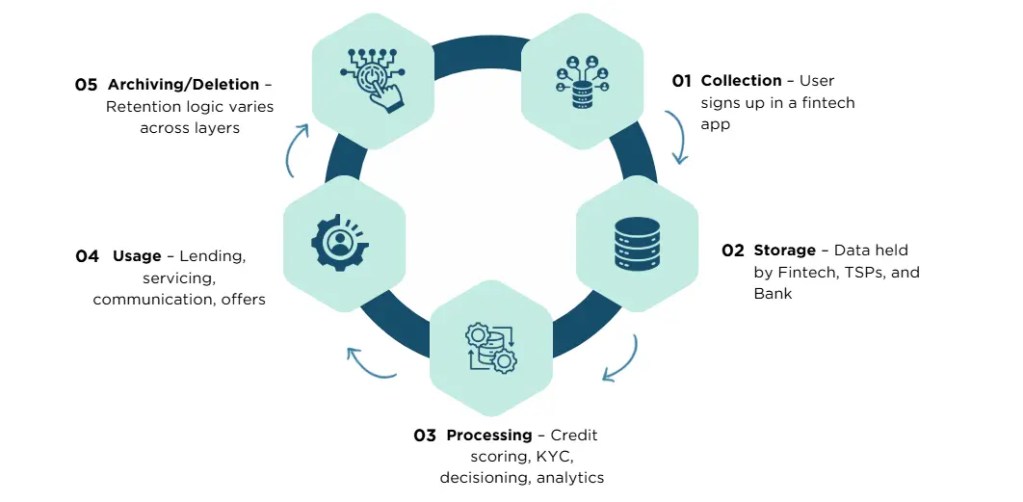

Managing data through the DPDPA lens means overseeing a comprehensive lifecycle: collection, storage, processing, usage, and deletion. Consider how a digital wealth management platform, acting as a TSP, collects client data through app interactions. They securely store this data in cloud environments and use it to tailor investment suggestions, all on behalf of the financial institution. Each phase demands adherence to purpose limitation and user consent, requiring embedded monitoring and contractually mandated controls. This lifecycle approach ensures no compliance gaps emerge during complex, multi-party financial transactions.

1. Collection Stage

Requirement: Explicit consent with clear purpose disclosure at point of capture

Operational Impact: Customer onboarding processes must be redesigned to capture granular, purpose-specific consent rather than blanket permissions

Success Metric: 100% traceable consent with zero ambiguous data collection instances

2. Storage Stage

Requirement: Secure storage limited to necessary duration with defined fiduciary-processor roles

Operational Impact: Legacy data warehouses require complete restructuring with automated retention enforcement

Success Metric: Zero over-retention incidents and complete data lineage visibility

3. Processing Stage

Requirement: Processing activities aligned exclusively with consented purposes

Operational Impact: Analytics, AI/ML models, and decision engines must operate within strict purpose boundaries

Success Metric: All processing activities mapped to specific consent instances with audit trails

4. Usage Stage

Requirement: Service delivery constrained to consent-defined boundaries

Operational Impact: Cross-selling, personalization, and communication strategies require consent verification before execution

Success Metric: Zero unauthorized usage incidents with full customer control

5. Archiving/Deletion Stage

Requirement: Automated deletion upon purpose fulfillment or consent withdrawal

Operational Impact: Systems must support immediate, verifiable data deletion across all environments

Success Metric: Complete data erasure within defined timeframes with cryptographic proof

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

The lifecycle approach must be embedded in every business process, technology system, and partner integration to prevent compliance failures that could result in significant regulatory and reputational consequences.

Embedding TSP Oversight: Contracts, Monitoring, and Accountability

Operational readiness extends governance beyond internal teams to encompass TSP partners. Roles, Data Fiduciary, Processor, or Sub-Processor, must be unambiguously identified and reflected in contracts that outline data use limits, consent management duties, breach protocols, and liabilities.

Continuous monitoring systems should aggregate logs from TSP platforms to alert on suspicious activities or retention violations. Periodic Data Protection Impact Assessments (DPIAs) help assess evolving third-party risks, transforming external dependencies into governance strengths that ensure transparency, regulatory confidence, and operational agility.

Key Roles & activities that a TSP shall have to provide under DPDPA:

- Process data only for the specified, consented purpose

- Ensure strong data security and access control mechanisms

- Delete or archive data as per agreed retention timelines

- Maintain processing logs for audit and compliance tracking

- Immediately halt data processing if consent is revoked

- Operate under binding contracts defining scope, liability, and compliance obligations

TSPs play a critical role in operationalizing DPDPA, and their compliance is essential for the fiduciary’s overall accountability.

From Compliance to Competitive Advantage

As BFSI organizations deepen collaboration with fintechs, TSPs, and embedded finance players, operationalizing DPDPA compliance across the entire data ecosystem becomes more than risk management, it becomes a market differentiator. Institutions embedding privacy-by-design and purpose limitation into every digital interaction consistently rank higher in customer trust surveys, face fewer regulatory interventions, and secure attractive partnerships.

For instance, a digital lending platform that captures transparent consent, vigilantly monitors data usage across TSPs, and strictly enforces data deletion not only sidesteps regulatory fines but earns a reputation as a privacy leader, fostering wider customer adoption.

Key Operational Challenges Emerging:

- Consent Gaps – Fintechs may collect user data without the bank’s ability to trace or validate consent, creating legal exposure.

- Over-retention and Storage Risks – PAN, Aadhaar, and KYC documents stored beyond their purpose validity pose serious storage and regulatory risks.

- Unauthorized Processing – Use of analytics SDKs or behavioral data for cross-selling or marketing without valid consent violates DPDPA principles.

- Processor and TSP Oversight – Data breaches or poor retention practices at the API or TSP layer make the Data Fiduciary liable for non-compliance.

- Transparency & Access Issues – When customers raise access requests via a fintech app, the bank must still be able to respond and show complete audit logs.

To operationalize DPDPA effectively, organizations must:

- Embed consent capture, audit logging, and deletion triggers across partner systems.

- Establish clear data processor contracts with TSPs that define purpose, retention, and breach handling.

- Ensure consistent retention logic and purpose tracking across all digital layers—fintechs, embedded flows, and core systems.

- Conduct DPIAs regularly to identify and mitigate risks like unauthorized sharing or misaligned data handling.

From Compliance to Competitive Advantage

To move beyond checklists toward embedded compliance, BFSI leaders must advance holistic governance that extends accountability across the entire data value chain, with special focus on TSPs who significantly expand compliance perimeters.

- Define Roles Clearly: Identify and document whether partners act as Data Fiduciaries, Processors, or Sub-Processors according to actual data control and usage purposes.

- Map Responsibilities: Ensure all parties understand and execute their privacy obligations, fiduciaries set purpose; processors act on instructions; subprocessors operate within limited scopes.

- Role-Aligned Contracts: Deploy agreements that clearly specify data handling, consent adherence, security duties, and breach response.

- Integrate DPDPA into TPRM: Align vendor risk frameworks with DPDPA, encompassing onboarding, ongoing performance, privacy monitoring, and offboarding.

- Maintain Centralized Vendor Inventory: Track all partners processing roles, risk ratings, and regulatory exposure in a living repository.

- Enable Auditability and Traceability: Build integrated systems logging data flows, access events, and processing activities across all roles to support DPIA and regulatory reporting.

Embedding these pillars transforms DPDPA into a strategic asset, reducing risks and fostering a culture of privacy-first innovation that builds lasting trust in India’s dynamic digital financial ecosystem.

The Path from Vision to Sustainable Growth

The journey from DPDPA principles to operational excellence demands a commitment by BFSI leaders to embed ecosystem-wide governance turning TSP partners from compliance exposures into collaborative data stewards. By interweaving detailed consent management, lifecycle discipline, and continuous partner oversight, organizations build resilient ecosystems aligned with regulatory mandates and customer rights.

This approach ensures institutions not only meet compliance obligations but also cultivate the trust and agility essential to thrive in India’s vibrant open data economy. The future belongs to those who master the connection between strategic vision and practical execution, which shall be shaping an innovative financial services landscape where privacy is foundational to competitive advantage.