The compliance environment for financial institutions is undergoing a fundamental transformation. As regulatory supervision intensifies and audit mechanisms become more intrusive, banks, NBFCs and other financial institutions are being held to far more dynamic and forward-looking standards of accountability. Compliance is no longer confined to internal controls or policy adherence or physical boundaries it now extends across ecosystems shaped by digital innovation, cloud-native infrastructures, and a growing network of third-party technology partners.

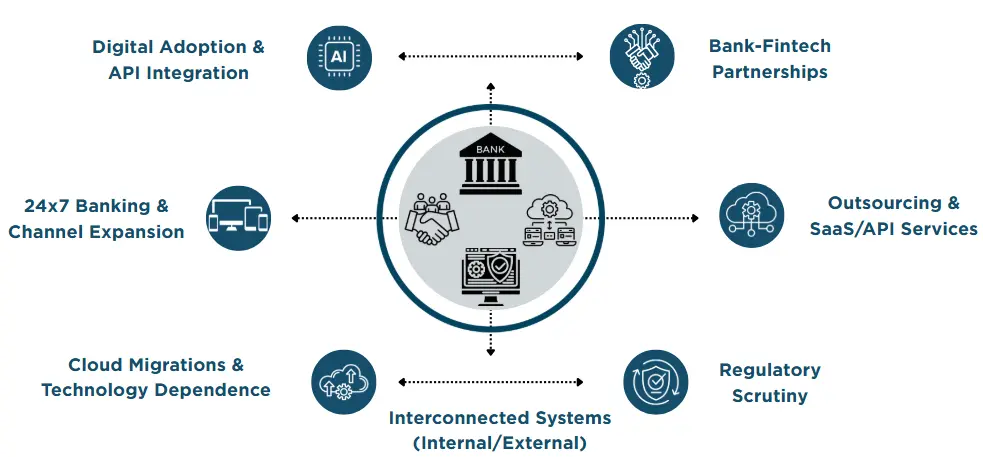

At the same time, the increasing entwinement between banks and non-banking players especially through embedded finance, co-lending models, and digital onboarding journeys has introduced new vectors of operational, data, and conduct risk. The velocity of technological adoption has outpaced traditional control frameworks, placing institutions in a delicate balancing act between innovation and regulatory rigor.

This shift is particularly challenging for small and mid-sized players especially middle-layer NBFCs who often operate under the same regulatory expectations but without equivalent access to budget, technology, or skilled compliance talent. While the compliance bar remains uniformly high, their ability to build integrated control systems or conduct proactive monitoring is often constrained by limited internal capabilities. For these institutions, the absence of structured frameworks and reliable partners makes compliance not only a burden but a growing risk.

This edition explores the compliance challenges that are not only evolving, but compounding often silently in modern banking and lending environments. For leaders steering their organizations through this complexity, early recognition and recalibration will be key.

Compliance Requirements Explosion: From Master Directions to Data Laws

As regulatory expectations grow sharper, banks and NBFCs are navigating a widening patchwork of directives, internal standards, and evolving obligations. The rise in consolidated Master Directions has added multiple layers of compliance across functions. In just the last few years, regulatory bodies have issued significant guidelines on Digital Lending, KYC updates, IT Governance, Outsourcing of Technology Services, and Operational Risk Management each introducing new control expectations, reporting formats, and governance requirements.

Newer legislations like the Digital Personal Data Protection Act (DPDPA) will further expand the compliance perimeter bringing areas like data governance, consent, and third-party processing into sharper focus.

With internal policies, risk controls, IT governance, and partner oversight now converging, few institutions are equipped to manage this complexity in silos. Banks and Financial institutions may need to put up an integrated framework to realign all compliance requirements to comply in a sustainable manner.

An Integrated Compliance Framework is essential one that unifies regulatory, operational, and policy oversight into a single, structured approach.

With the influx of revised Master Directions, emerging data privacy laws like DPDPA, and the overlay of industry standards and internal policies, the compliance ecosystem has grown increasingly complex, decentralized, and fragmented.

Relying on siloed audits, reactive reporting, or isolated control implementations is no longer sustainable. Financial institutions must pivot towards an Integrated Compliance Framework (ICF) a consolidated governance architecture that streamlines oversight, reduces redundancy, and enables risk-aligned decision-making across the enterprise.

The ICF approach brings together regulatory requirements, internal policies, risk controls, and third-party compliance obligations into a unified, actionable structure. It allows for:

- Real-time compliance visibility, not post-facto reconciliation

- Consolidated reporting across multiple guidelines and standards

- Resource optimization by eliminating duplicative assessments and siloed reviews

- Enhanced transparency through consistent control testing and accountability mapping

- Improved board-level insights into enterprise-wide compliance health

ICF implementation progresses through stages from manual processes to fully optimized GRC systems

The framework supports integration with digital lending norms, IT outsourcing mandates, cybersecurity standards, and internal governance layers

A unified reporting and audit engine enables organizations to measure readiness across both regulatory and business alignment parameters

Adopting ICF is not just about simplifying compliance it’s about future-proofing governance structures and embedding resilience into the operational fabric of banks and NBFCs.

Rapid Evolution of Products and Customer Journeys: The Compliance Catch-Up

The pace at which financial products, services, and digital interfaces are evolving has outstripped the traditional compliance design process. With continuous enhancements in digital lending models, customer onboarding flows, embedded journeys, and API-led products, regulatory obligations are no longer static they are dynamic and deeply intertwined with user interactions.

Key processes like KYC, DLG (Digital Lending Guidelines), account aggregation, and real-time credit assessments demand precise, real-time compliance mapping. However, most institutions continue to face challenges such as:

- Fragmented ownership of customer journeys across teams and platforms

- Inconsistent regulatory interpretation during product rollouts

- Delayed compliance validations that occur post go-live

- Inability to map controls directly to each customer interaction or digital event

- Front-end compliance often being well-orchestrated, while backend processes remain broken, manual, and disconnected from control frameworks

This complexity is further amplified in co-lending setups, embedded finance partnerships, and marketplace models where the financial product is often invisible to the end-user but still subject to regulatory scrutiny.

To navigate this fluid environment, institutions must move towards a journey-based compliance approach one that aligns controls to each stage of the customer lifecycle from front-end to back-end of processes rather than generic checklists. This includes:

- Embedding compliance gates within each journey (onboarding, underwriting, disbursal, servicing)

- Mapping data capture, risk checks, and disclosures directly to customer actions

- Automating exception handling and audit trails at a journey level

- Coordinating compliance ownership across product, tech, legal, and ops

Moreover, with the rise of outsourced processes and third-party dependencies, institutions are also expected to ensure that regulatory accountability extends beyond organizational boundaries.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

Leaving Compliance Requirement to Fintechs and Thirdparties

As banks and NBFCs continue to deepen their partnerships with fintechs and tech service providers, many mistakenly assume that regulatory compliance can be delegated alongside the function. Whether it’s onboarding journeys, credit scoring models, or customer communication tools compliance responsibility cannot be outsourced.

Fintech and Embedded Finance Mode

In Fintech and embedded finance partnerships, fintechs may originate the journey, but the compliance responsibility stays with the bank or NBFC. Regulatory accountability cannot be offloaded.

Tech & Third-Party Platforms

The rise of API providers, SaaS tools, and cloud platforms has expanded reliance on external partners. But even with outsourced execution, compliance must remain institution-owned and closely governed.

Regulators expect the regulated entity to maintain full accountability, regardless of who executes the process. This makes it imperative to embed compliance checks not just within the product, but also during partner onboarding and integration.

Institutions must:

- Evaluate third-party controls before integration

- Map regulatory requirements to each outsourced activity (KYC, consent, scoring, data sharing)

- Ensure contractual clarity on compliance obligations

- Monitor partners continuously, not just at onboarding

Building compliance at the design level across both internal and partner ecosystems is no longer optional, but essential for operational resilience and regulatory trust.

The Missing Metrics in Compliance Programs

Many institutions, especially smaller NBFCs, still rely on periodic checklists and manual validations lacking a structured, KPI-driven framework to monitor compliance performance. Without quantifiable metrics, risk signals remain invisible until too late.

Institutions must define compliance KPIs aligned to key journeys onboarding accuracy, KYC rejection rates, consent capture quality, turnaround time on dispute resolution, etc. and track them consistently.

Moreover, mapping the right compliance skills to each journey is critical. Smaller NBFCs often lack in-house capability and should onboard trusted partners with domain expertise, clear SLAs, and accountability matrices. Whether outsourced or internal, each process must be mapped back to a regulatory obligation, measured via pre-defined metrics, and monitored in real-time.

Even as institutions strengthen processes and adopt frameworks, foundational challenges persist—many of which are often overlooked but carry significant risk implications.

Key issues include:

Lack of a comprehensive understanding of compliance requirements across departments, leading to fragmented ownership and inconsistent implementation

Limited adoption of global standards such as ISO 27001, ITIL, and COBIT, which are essential for structured control environments

Absence of a top-down compliance culture, where governance is viewed as an operational requirement rather than a board-level priority

Without strategic direction, institutional awareness, and alignment to industry standards, even the most advanced tools or frameworks will fall short.