Most compliance failures aren’t policy issues - they’re execution gaps. Learn why compliance breaks on the ground and how to...

Know moreBenchmarking Digital Home Loans: Elevating Customer Journeys for Market Growth

The Evolving Home Loan Landscape

India’s home loan sector is experiencing a major transformation, driven by rapid urbanization, rising disposable incomes, and increasing demand for home ownership. The market has witnessed robust growth, with outstanding home loans nearly doubling from ₹17.95 trillion in FY19 to ₹33.34 trillion in FY24. Housing finance now accounts for 47% of all retail credit, underlining its significance in India’s financial ecosystem.

However, despite this expansion, the country faces a housing shortage of nearly 100 million units, primarily in the affordable segment. Government initiatives like Pradhan Mantri Awas Yojana (PMAY) have encouraged first-time homebuyers, but challenges in affordability, credit access, and process inefficiencies persist. Traditional home loan journeys remain complex, time-consuming, and heavily reliant on offline processes, making digital transformation a critical need for lenders aiming to scale efficiently.

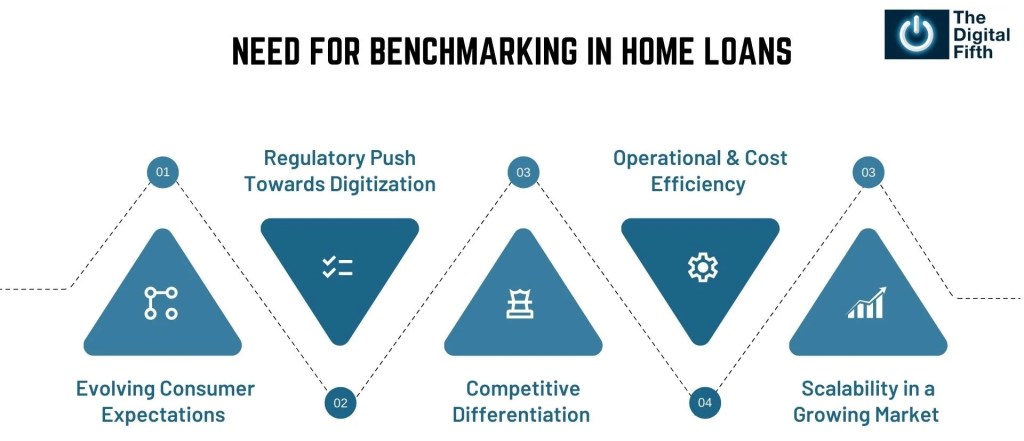

Need for Benchmarking in Home Loans

The home loan industry has traditionally prioritized risk mitigation and regulatory compliance, leading to structured but often complex lending processes. While significant progress has been made in digital adoption, enhancing process efficiency, customer satisfaction, and market penetration remains a key focus area.

Evolving Consumer Expectations – Borrowers today expect quicker, paperless loan approvals, similar to other retail financial products. Financial institutions adopting digital innovations have seen a competitive edge in acquisition and engagement.

- Regulatory Push Towards Digitization – Compliance measures such as eKYC, Account Aggregator (AA), and digital property verification are being encouraged to enhance accessibility, making benchmarking essential for aligning with regulatory expectations.

- Competitive Differentiation – With new-age fintechs and digital-first lenders gaining traction, established institutions are increasingly evaluating how their home loan journeys compare in terms of efficiency, automation, and customer experience.

- Operational & Cost Efficiency – Automated underwriting, AI-driven risk models, and digital disbursal mechanisms are streamlining processes for some players, while others continue refining their transition to digital-first lending.

- Scalability in a Growing Market – As housing finance now comprises 47% of retail credit and home loan portfolios exceed ₹33.34 trillion (FY24), the ability to meet demand efficiently depends on benchmarking against scalable industry best practices.

Through systematic benchmarking, financial institutions can continuously refine their digital adoption strategy, eliminate inefficiencies, and enhance competitiveness in the evolving home loan ecosystem.

While technology has made strides in simplifying home loan applications, several hurdles prevent a fully digital, frictionless experience:

- Fragmented Land Records & Legal Verification

Property ownership verification remains a major bottleneck due to the lack of a centralized, digitized land registry across India. Many states have inconsistent land records, requiring extensive manual due diligence to confirm ownership, check for encumbrances, and validate titles. This delays approval timelines and introduces inefficiencies that prevent true end-to-end digitization. - Offline-Dependent Property Valuation

Unlike unsecured loans, home loans require lenders to assess the property’s market value and condition before sanctioning the loan. Currently, this process depends on physical inspection by a surveyor, followed by a manually generated report. While Automated Valuation Models (AVMs) and AI-powered valuation tools are emerging, they are not yet widely adopted or fully reliable. This offline dependency slows down the digital lending journey. - Manual Underwriting & Document Handling

Home loans involve extensive documentation, including income proofs, property papers, and credit checks, which often require physical verification. Despite advancements like eKYC, DigiLocker, and Account Aggregator frameworks, lenders still rely on manual review processes. Many applications require customers to visit branches for document submission or clarifications, increasing turnaround times and adding friction. - Legacy Core Systems & Limited Automation

Many financial institutions continue to operate on outdated loan origination and underwriting systems, making integration with new-age digital platforms difficult. While fintechs and new-age lenders have introduced faster, automated underwriting systems, traditional banks and NBFCs struggle with legacy infrastructure. This limits the ability to offer instant approvals, real-time tracking, and seamless loan disbursal. - Low Customer Trust in Fully Digital Processes

Home loans are high-value, long-term commitments, and many borrowers—especially in Tier-2 and Tier-3 cities—prefer some human intervention in the approval process. While digital platforms have simplified application and onboarding, borrowers still seek offline touchpoints to clarify doubts and gain confidence in large financial transactions. This trust deficit prevents complete digital adoption.

Bridging Online & Offline: The Role of a Phygital Approach

Given these challenges, a fully digital home loan journey isn’t yet practical. Instead, lenders must embrace a phygital (physical + digital) approach, blending online convenience with strategic offline interventions to ensure speed, transparency, and customer trust.

- Digital Pre-Approval & Eligibility Checks: Customers can apply online, verify credit scores, and receive instant eligibility confirmation.

- Seamless Document Collection & eKYC: Lenders can integrate DigiLocker, Aadhaar-based verification, and e-signature solutions to reduce paperwork.

- Tech-Assisted Property Valuation: AI-driven valuation tools can complement physical surveys to accelerate assessment.

- Human Assistance at Key Touchpoints: Video KYC, branch-assisted support, and doorstep service for document pickup can provide personalized engagement where needed.

By integrating automation, AI-driven risk assessment, and minimal manual interventions, lenders can create hybrid home loan journeys that maximize efficiency while ensuring trust and compliance.

Unlocking Market Potential Through Benchmarking & Digital Optimization

Key Areas for Benchmarking Digital Home Loan Journeys

1. Loan Origination & Customer Onboarding

- Current Landscape: The adoption of pre-filled applications using Account Aggregator (AA), CKYC, and credit bureau data is streamlining borrower onboarding.

- Optimization Strategies: AI-based underwriting and instant eligibility checks are reducing manual dependencies and improving speed.

2. Property & Legal Verification

- Current Landscape: Variability in land record digitization impacts verification timelines, necessitating manual interventions in several cases.

- Optimization Strategies: AI-driven land record analytics, blockchain-based property registries, and API integrations with government data sources are emerging as potential enablers.

3. Credit & Risk Assessment

- Current Landscape: While many lenders have integrated AI-based credit scoring and alternative data models, manual document verification remains a step in certain cases.

- Optimization Strategies: Real-time document verification using OCR, DigiLocker, and biometric validation is driving efficiency in credit assessment.

4. Customer Communication & Transparency

- Current Landscape: While many lenders provide basic application tracking, real-time, proactive updates across digital channels are emerging as a differentiator.

- Optimization Strategies: Automated alerts via WhatsApp, SMS, and mobile apps, coupled with borrower dashboards, are elevating transparency.

5. Loan Disbursement & Post-Sanction Services

- Current Landscape: While e-signatures and digital agreements are improving TATs, certain approvals still involve manual interventions.

- Optimization Strategies: API-based automated disbursal workflows and faster fund transfers are accelerating the final stages of loan processing.

The Role of The Digital Fifth’s PULSE Framework

To improve digital lending experiences, The Digital Fifth’s PULSE Framework provides a structured approach:

Conclusion: The Digital Advantage in Home Loans

The future of home loans lies in seamless, digital-first experiences. By bridging online and offline processes, leveraging automation, and using benchmarking frameworks like PULSE, lenders can unlock massive growth, improve customer satisfaction, and enhance operational efficiency. The home loan sector is evolving—those who embrace digital transformation will lead the way in expanding saving costs, market penetration and making home ownership more accessible than ever.

RELATED POSTS

The Corporate Card Opportunity Nobody’s Talking About | The Next B2B Fintech Infrastructure Play

Corporate cards for SMEs could become the next major fintech infrastructure play. Explore how B2B cards, spend management platforms, and...

Know more

Data Readiness in BFSI: Building the Intelligence Layer for AI

India’s BFSI sector is shifting from data accumulation to intelligence-ready infrastructure. Explore how real-time pipelines, lakehouses, and governance power AI.

Know more