Table of Contents

Introduction

When fintech first gained momentum in the early 2010s, the vision was clear: unbundle the complex giant – The bank. The goal was to free customers from the rigidity of traditional banking structures and deliver financial services that were flexible, personalized, and customer-first.

More than a decade later, we are in the age of integration and collaboration. Banks are not only partnering with fintechs but also investing in them. Fintechs, in turn, are acquiring peers to expand their capabilities. Innovations like UPI have blurred the boundaries even further, enabling banks and fintechs to co-create offerings at scale.

Bank + Fintech Collaboration

At the heart of this rebundling is the customer. Partnerships that endure are the ones that move beyond transactional efficiency and focus on transparency, fairness, and seamless experiences. This requires banks and fintechs to design with compliance and customer sovereignty as non-negotiables, not afterthoughts.

Embedding Compliance as the Foundation for Bank–Fintech Collaboration

The regulatory climate in India is evolving rapidly, digital lending, BNPL, and credit cards have already seen guidelines from the RBI for better customer engagement & support to business models. For collaborations to thrive, compliance cannot be an afterthought. It must be embedded at the blueprint stage.

The revised RBI’s Digital Lending Guidelines (DLG) of 2025 mandate complete transparency, customers see all matched and unmatched loan offers, ensuring fairness and eliminating bias. Similarly, the Digital Personal Data Protection Act (DPDPA) makes data privacy central to all customer interactions.

For partnerships to thrive, compliance has to be more than a checkbox, it must shape product design.

Patterns That Work

Over the course of working with multiple bank-fintech partnerships, we’ve seen a few recurring patterns emerge. These are practical lessons, insights from collaborations that managed to balance speed with stability, and innovation with compliance.

Join Our Newsletter

Get exclusive insights on banking, fintech, regulatory updates and industry trends delivered to your inbox.

- 1. Clear Role Definition

- Fintechs should focus on frictionless onboarding, intuitive journeys, and customer-first design.

- Banks/NBFCs must anchor scale, regulatory assurance, and operational reliability.

- 2. Customer-Centric Orchestration

The most successful partnerships practice “Customer Sovereignty” where transparency becomes a core value proposition, not just compliance. Modern borrowers demand clarity on salary credits, loan status, and account balances. Partnerships that recognize this reality win customer loyalty and lifetime value.

- 3. Compliance-First Design

- Fees and Charges Within Norms: Interest rates, minimum balance, fees, and charges ancillary costs should not only comply with regulatory caps but also be disclosed upfront.

- No Dark Patterns: Borrowers should never feel nudged or misled into decisions. Customer flows need to empower informed choices rather than conceal critical details.

- 4. Optimized API integrations

API latency is one of the most common reasons customers abandon digital journeys. High latency causes frustrating delays, repeated attempts, and ultimately customers drop-off from the journey despite having clear intent to complete it.

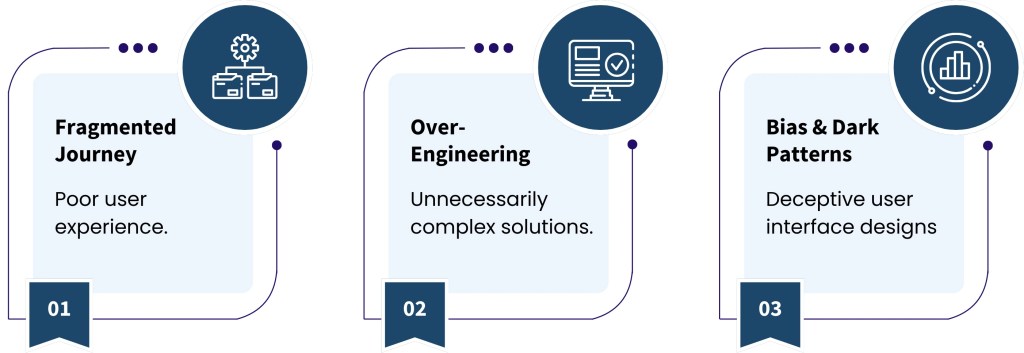

Common Pitfalls in Bank–Fintech Partnerships

Just as there are patterns that drive success, there are also pitfalls that repeatedly undermine partnerships. These challenges are avoidable, yet many collaborations fall into the same traps, often by prioritizing speed over coherence or by overlooking the basics of user trust.

- Fragmented Journeys: When customer journeys are split between bank and fintech without tight integration, drop-offs rise sharply. For example, a customer who starts onboarding in-app but is redirected to a clunky bank interface often abandons the process. Seamless handoffs, consistent branding, and unified support are essential to prevent friction.

- Over-Engineering: Partnerships sometimes try to launch with a “super app” mindset, loading too many features upfront. Lean MVPs, such as simple current or savings accounts with smooth onboarding, win adoption faster. Additional services can be layered in later.

- Bias & Dark Patterns Design nudges that favor one lender, hide true costs, or complicate repayment erode trust. With RBI’s increasing focus on fair disclosures, even the perception of bias can invite scrutiny. Radical transparency, where the customer feels empowered, not steered, is the winning approach.

The Future of Bank–Fintech Collaboration

The evolution ahead promises deeper integration through multiple collaboration models:

- Strategic Ecosystem Models: From strategic alliances and joint ventures to white-label solutions and open banking frameworks

- AI-Driven Success Orchestration: Beyond risk assessment, AI will optimize for customer financial success while ensuring regulatory compliance and risk management as the bedrock

- Agile-Native Development: Iterative development methodologies enabling continuous improvement and rapid market adaptation

Strategic Imperative: Partnership as Platform Strategy

The financial services industry is experiencing its most significant transformation since electronic banking. The question isn’t whether to partner. The question is how to partner in ways that create sustainable competitive advantage.